What is the Impact of 2026 Auto-Insurance Regulatory Changes on Chiropractic Liens?

The 2026 auto-insurance regulatory changes rewrite how chiropractic personal injury liens get documented, submitted, and paid. These aren't compliance tweaks. They target the pressure points where chiropractic care already faces the most scrutiny: medical necessity justification, billing code specificity, and documentation standards that separate active treatment from maintenance care.

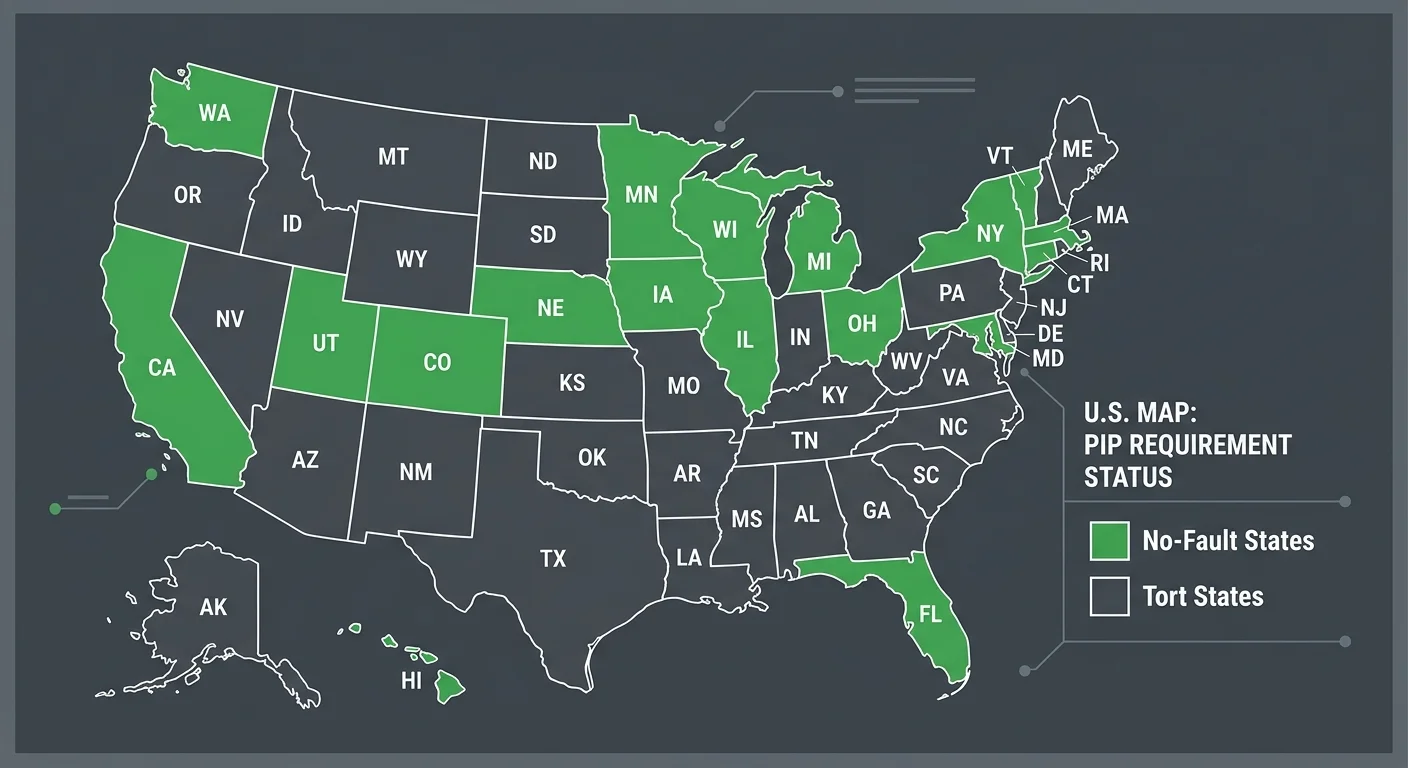

The U.S. auto insurance market is projected to hit $367.5 billion by 2026. The regulatory shifts driving that growth prioritize claim deflection over care reimbursement. Approximately 12 states require Personal Injury Protection (PIP), and most are tightening evidentiary requirements for what qualifies as medically necessary treatment. Maintenance care isn't covered under most auto policies. The 2026 rules demand more granular documentation to prove active treatment status.

Lien recovery now requires stronger clinical narratives, more detailed progress notes, and appeals that argue medical necessity instead of resubmitting the same claim with louder font. Rear-end collisions account for nearly 29% of all crashes. Whiplash injuries are a core revenue driver for chiropractic PI work. But the average denial rate for medical claims already sits between 5% and 10%. Complex PI cases run higher. The 2026 changes push that rate further unless the practice has a billing partner who knows how to construct a defensible lien argument.

The settlement timeline for a personal injury claim runs from a few months to over a year. Every month of delay compounds cash flow pressure. For car accidents with minor to moderate injuries like whiplash, settlements average between $15,000 and $30,000. That revenue disappears if the lien documentation fails under the new scrutiny.

Software can submit a claim. It can't argue one. That distinction defines which chiropractic practices protect their PI revenue in 2026 and which watch it evaporate under regulatory pressure they didn't see coming.

Last Updated: May 23, 2026

- Why the 2026 Regulatory Shift Matters for Chiropractic Practices

- How State-Specific PIP and Lien Laws Complicate the Picture

- What Automated Billing Systems Can't Handle

- How to Prepare Your Practice for the 2026 Changes

-

Frequently Asked Questions

- Why do PI liens take longer to settle than standard chiropractic claims?

- How do state-specific PIP and lien laws impact practice revenue?

- What kind of documentation will be most critical for chiropractic liens under the 2026 regulations?

- How can my practice prepare for shifts in auto-insurance reimbursement and documentation rules?

- Will the 2026 regulatory changes affect MedPay claims differently than third-party liability claims?

- What is the biggest financial risk for chiropractors when managing their own auto accident liens?

- What This Means for Your Practice

Why the 2026 Regulatory Shift Matters for Chiropractic Practices

You need to see why this shift targets the exact claims that keep PI revenue stable.

The 2026 regulations aren't a compliance update.

They're a triage test.

Auto insurers are betting that tighter documentation requirements will deflect enough claims to offset adjudication costs. They're counting on practices to fail. And the billing partners who survive this shift will be the ones who understand chiropractic documentation—not just submission speed.

The practices most vulnerable? The ones treating the highest volume of rear-end collision injuries.

These cases—accounting for nearly 29% of all crashes—produce the most consistent chiropractic revenue. And they're the first targets for heightened scrutiny.

The Documentation Chasm

Here's the problem most practices don't see.

The 2026 rules demand clinical narratives that distinguish active treatment from maintenance care at every visit. That distinction determines whether your lien gets paid or abandoned.

Approximately 12 states require PIP coverage. Those states are leading the charge on medical necessity documentation standards.

The new requirements don't just ask for diagnosis codes. They require visit-by-visit progress documentation, objective findings tied to functional improvement, and explicit justification for continued care.

Most chiropractic EHR templates weren't built for this.

The software prompts providers to check boxes and copy forward notes. That workflow produces documentation that reads like maintenance care—even when the treatment is active and medically necessary.

Software can't argue the difference. Your billing partner has to.

Medical Necessity Arguments Under the New Rules

So what does a medical necessity argument look like under the 2026 standards?

It's not a resubmission.

It's a constructed clinical narrative. One that connects initial injury presentation to measurable functional deficits, ties each visit to documented progress (or lack thereof), and explains why ongoing treatment remains medically justified.

The American Chiropractic Association publishes clinical guidelines that define best practices for documentation and care planning.

Those standards form the foundation of a defensible lien argument. But guidelines don't write appeals. People do.

And this is where personal injury (PI) lien billing separates into two paths.

One is managed by software that resubmits the same claim until the appeal window closes. The other is managed by a billing partner who reads the chart, understands the denial reason, and constructs the argument that gets the claim paid.

| Regulatory Change | Documentation Impact | Revenue Risk |

|---|---|---|

| Stricter medical necessity thresholds for PIP and third-party liability claims | Visit-by-visit progress documentation required; objective findings must tie to functional improvement and justify continued care | Claims that read as maintenance care—even when treatment is active—face automatic denial or adjuster challenge |

| Heightened scrutiny on whiplash and soft-tissue injury claims | Clinical narratives must distinguish acute treatment from chronic management at every encounter; EHR templates designed for compliance checkboxes fail this test | Rear-end collision cases—the highest-volume PI revenue source—become the first targets for deflection under the new rules |

| Expanded evidentiary requirements for lien perfection in no-fault states | Documentation must include initial injury presentation, measurable deficits, treatment plan rationale, and visit-specific progress notes that support ongoing medical necessity | Liens filed without this level of specificity lose priority in settlement negotiations or are excluded entirely |

| Tighter timelines for denial appeals and supplemental documentation requests | Practices must respond with constructed clinical arguments—not resubmissions—within compressed windows; software cannot write these appeals | Every missed appeal window converts recoverable revenue into write-off; cash flow pressure compounds across multiple open liens |

| State-by-state divergence in PIP benefit caps and documentation standards | National billing partners operating volume-first models cannot scale specialty knowledge across conflicting state requirements; chiropractic-specific rules are deprioritized or ignored | Practices in high-scrutiny states lose revenue to partners who treat all states identically |

How State-Specific PIP and Lien Laws Complicate the Picture

Federal visibility doesn't override state-level insurance structures.

And that's where the complexity multiplies.

Approximately 12 states require Personal Injury Protection (PIP) insurance as part of their no-fault auto insurance laws. The rest run tort systems where third-party liability determines who pays.

Your lien recovery strategy isn't universal. It's dictated by which system governed the accident.

And the 2026 regulations won't standardize these frameworks. They'll layer new documentation requirements on top of existing state-level variation.

A billing partner who treats PIP claims in Florida the same way they treat liability claims in Texas isn't billing. They're guessing.

No-Fault vs. Tort States

No-fault states limit your ability to pursue third-party claims until PIP benefits are exhausted or the injury meets a statutory threshold.

That threshold varies wildly. Some states use verbal descriptors like "permanent injury." Others set benefit caps that determine when a patient can step outside no-fault and file a liability claim.

Tort states let you file a lien against the at-fault driver's liability insurance immediately. No PIP exhaustion requirement.

But settlement timelines stretch from a few months to over a year. And liability carriers aggressively challenge medical necessity on chiropractic claims.

So your billing partner needs to know which rules govern the claim before they touch the file.

Volume-first billing companies don't build workflows around state-specific PIP and lien laws. They build workflows around throughput.

That's where lien revenue dies quietly.

PIP Exhaustion and Lien Priority

Here's the thing: PIP exhaustion doesn't mean the patient ran out of coverage and walked away.

It means the no-fault benefits are fully used and the claim can now convert to a third-party lien. That conversion is a documentation trigger. And it's exactly where generalist billing companies lose the thread.

Once PIP is exhausted, your lien enters a priority queue alongside other medical providers, attorney fees, and sometimes statutory caps on total recovery.

The carrier will challenge every line item that isn't tied to acute care or functional restoration. Maintenance visits get cut. Passive modalities get questioned. Anything that looks like wellness care becomes a negotiation point.

But automation can't argue lien priority.

Software can't explain why 12 weeks of manipulation was medically necessary when the adjuster's internal guideline says 6. That argument requires a human who understands chiropractic scope, documentation standards, and how to frame causation in a way that survives legal review.

The 2026 regulations will make that argument harder. Not easier.

| State Type | PIP Requirement | Lien Recovery Model | 2026 Compliance Burden |

|---|---|---|---|

| No-Fault PIP State | Mandatory PIP coverage | Submit to patient's own insurer first; lien shifts to third-party liability after PIP exhaustion | Requires dual documentation strategy—PIP exhaustion tracking plus tort liability narrative for post-cap treatment |

| Tort Liability State | No PIP requirement | Lien submitted directly to at-fault driver's liability carrier or uninsured motorist coverage | Requires fault establishment before payment; longer settlement timelines demand stronger medical necessity arguments upfront |

| Choice No-Fault State | Optional PIP election | Recovery model depends on patient's policy selection at time of accident | Billing partner must verify coverage type before filing; documentation requirements vary by patient policy election |

| Add-On PIP State | PIP available but tort claims allowed simultaneously | Lien can pursue PIP and third-party liability concurrently | Highest documentation complexity—must satisfy both PIP medical necessity standards and tort causation arguments in parallel |

What Automated Billing Systems Can't Handle

But regulatory complexity isn't the failure point.

The failure point is what happens when the system hits a scenario it wasn't programmed for.

Automated billing platforms process clean claims at scale. Submission speed is the metric. Code compliance for straightforward cases happens without friction.

Personal injury liens under the 2026 regulatory environment aren't clean claims. They're contested revenue. Every stage requires human judgment.

Software identifies a denial code. It can't read a chart, assess whether the documentation supports medical necessity, and construct an appeal that addresses the insurer's specific objection.

That gap is where practices lose recoverable PI revenue. The 2026 changes make that gap wider.

Why Volume Models Deprioritize High-Friction PI Liens

Here's what most practices don't understand about why most billing companies abandon complex claims.

Volume-first billing models measure success by claims submitted per hour. The economic model works when clean claims clear in days. When denials resolve with a single resubmission.

PI liens don't fit that workflow. The settlement timeline runs a few months to over a year. The work required to recover that revenue — documentation review, insurer negotiation, multi-step appeals — costs more in staff time than a volume model budgets for.

So the system flags the claim as low priority and moves on.

And that's the structural problem.

High-friction claims are the ones worth the most to your practice. They're also the first ones a volume biller deprioritizes because the cost to work them doesn't fit the throughput model. You never see that revenue disappear. The system just stops following up.

The Appeal Gap

The average denial rate for medical claims sits between 5% and 10%. Complex PI cases run higher under the new documentation standards.

Every denial that goes unworked is recoverable revenue aging past the appeal window.

So what does an effective appeal look like?

It starts with understanding the mechanics of a medical lien and why the insurer denied it in the first place. The denial reason isn't random. It follows a pattern. Active care documented as maintenance care gets denied. Treatment extending beyond typical recovery timelines without objective progress markers gets denied. Claims missing visit-specific functional improvement notes get denied.

The average denial rate for medical claims sits between 5% and 10%. Complex PI cases run higher under the new documentation standards.

An automated system resubmits the same claim with the same documentation.

A human-led billing partner reads the denial, reviews the clinical record, identifies the gap, and constructs the narrative that connects your documentation to the insurer's reimbursement criteria. That difference is the appeal gap. And under the 2026 standards, it's the gap between getting paid and writing off the claim.

| Claim Type | Automation Success Rate | Human Expertise Required | Typical Deprioritization Point |

|---|---|---|---|

| Clean claim (standard diagnosis, typical visit frequency, well-documented) | High — automated systems process these efficiently | Minimal — software handles submission and routine follow-up | Rarely deprioritized — fits the throughput model |

| Denied claim requiring documentation correction (missing modifier, incomplete progress notes) | Moderate — software flags the error but cannot assess clinical context | Moderate — human review required to determine whether chart supports resubmission or needs provider correction | Deprioritized after first resubmission attempt if denial persists |

| Medical necessity challenge (insurer questions treatment duration or frequency) | Low — software cannot construct clinical justification or argue care progression | High — requires chart review, narrative construction, and multi-step appeal | Deprioritized immediately in volume-first models due to staff time cost |

| PIP exhaustion transition to third-party liability (requires shift in documentation strategy mid-case) | Very low — automated systems do not track state-specific exhaustion triggers or adjust filing strategy | Critical — human expertise required to recognize exhaustion, refile correctly, and preserve lien priority | Deprioritized or missed entirely — system continues submitting to exhausted PIP until denials accumulate |

| Multi-party liability lien with settlement negotiation (attorney involved, disputed fault, contested care necessity) | None — automation cannot negotiate, assess settlement offers, or argue lien priority | Critical — full human-led strategy required from filing through settlement distribution | Abandoned in volume models — settlement timeline and negotiation cost exceed throughput economics |

How to Prepare Your Practice for the 2026 Changes

The 2026 regulations aren't a compliance update.

They're a triage test.

Billing partners who understand chiropractic documentation survive. Software platforms that only understand submission speed don't.

So what do you do about it?

Here's what preparation looks like before the 2026 regulations hit.

Audit Your Current PI Documentation

Pull every active PI lien file you have. Look at what you're submitting right now—the narrative reports, the exam findings, the treatment plans that justify medical necessity. Not what you think you're submitting. What's actually going out.

If your notes don't clearly separate active care from maintenance, they're already vulnerable. If they lean on generic templates that don't tie findings to a specific accident mechanism, those files won't survive the 2026 changes. They'll get rejected—and you won't have a defense.

This isn't about passing an audit. It's about protecting revenue on claims that take anywhere from a few months to over a year to settle—and that average between $15,000 and $30,000 for the whiplash and soft-tissue cases your practice sees every week.

Evaluate Your Billing Partner's PI Expertise

Ask your billing company one question: who handles your PI lien appeals when an adjuster rejects medical necessity? If the answer is 'our software flags it' or 'we escalate it back to you,' you don't have a billing partner. You have a clearinghouse.

The complexity of how complex PI liens are settled demands human judgment at every stage. Someone who knows how to read a patient file, construct a medical necessity argument, and appeal a denial using chiropractic-specific clinical reasoning.

Automation processes clean claims.

It abandons the messy ones—the exact claims where your practice loses the most revenue.

| Preparation Step | Timeline | Outcome if Skipped |

|---|---|---|

| Audit current PI documentation against 2026 medical necessity standards | 90 days before enforcement | First-wave denials with no time to revise clinical workflows before liens are filed |

| Update EHR templates to capture visit-specific functional improvement markers | 60 days before enforcement | Documentation reads as maintenance care even when treatment is active—automatic denial under new criteria |

| Train providers on objective progress documentation tied to ROM, pain scales, and ADL changes | 60 days before enforcement | Notes lack the specificity insurers demand—claims age past appeal window before the gap is identified |

| Evaluate billing partner's PI expertise and multi-step appeal process | 90 days before enforcement | Volume-first biller deprioritizes complex appeals—recoverable revenue dies in the system with no follow-up |

| Establish internal lien priority tracking workflow for PIP exhaustion and state-specific filing deadlines | 30 days before enforcement | Lien filed late or to wrong coverage layer—your claim drops below attorney fees and other providers in settlement order |

| Run test cases through new appeal workflow to identify documentation gaps before live claims | 30 days before enforcement | First real denial exposes a systemic documentation failure that affects every open PI case—backlog becomes unrecoverable |

Frequently Asked Questions

You've heard the warning. Now here are the objections.

These aren't academic questions. They're the friction points that determine whether your PI billing protects revenue—or erodes it while you wait for settlements that never arrive at full value.

Why do PI liens take longer to settle than standard chiropractic claims?

Standard insurance claims resolve in days or weeks. The insurer, the provider, and the patient are all identified at service. There's no dispute over liability.

PI liens sit in a different queue.

The settlement timeline can stretch from a few months to over a year because the at-fault party's insurer doesn't pay until liability is established, comparative fault is resolved, and the overall settlement is negotiated. Your lien priority gets subordinated to that timeline. And if your billing partner isn't tracking it, the claim ages silently while you assume it's being worked.

That's the structural difference.

Standard claims have a clear payer and a defined adjudication window. PI liens have a contingent payer, a contested liability framework, and no guarantee the settlement covers the full value of your care.

The longer the timeline, the more documentation gaps compound. And the more likely your biller deprioritizes the claim because the cost to recover it exceeds their throughput model.

How do state-specific PIP and lien laws impact practice revenue?

State frameworks determine how much of your revenue is recoverable and how fast you get paid. The variation isn't minor. It's the difference between direct PIP reimbursement within weeks and third-party lien recovery that takes months with no guarantee of full payment.

No-fault states with PIP coverage pay chiropractic claims directly up to the policy limit. Often without requiring liability determination. That's predictable revenue.

But once PIP exhausts, you're filing a lien against the at-fault party's settlement. And that's where state-specific lien priority laws dictate whether your claim gets paid in full, reduced, or subordinated to other creditors.

So your practice's PI revenue isn't just a function of the care you provide.

It's a function of the state framework governing how that care gets reimbursed—and whether your billing partner understands the nuances of PIP exhaustion, lien attachment, and priority rules in your jurisdiction.

Generalist billers treat every state the same. Vertical specialists know which claims to prioritize based on the state's lien hierarchy.

What kind of documentation will be most critical for chiropractic liens under the 2026 regulations?

Objective functional improvement markers tied to specific visit dates. Not narrative summaries. Not EHR-generated progress notes that read the same across 12 visits.

The 2026 standards tighten the definition of active care versus maintenance care. And the documentation that survives scrutiny will be the kind that explicitly connects each visit to measurable progress.

ROM improvements with specific degree measurements. Pain scale reductions documented visit-over-visit. Activities of daily living the patient couldn't perform at baseline and can perform now. All of it timestamped and tied to the treatment plan.

And here's the part most practices miss.

The documentation standard isn't what your state board requires for licensure. It's what the insurer's medical necessity review team will accept under the tighter 2026 framework.

If your notes don't prove continued active care with objective markers, the insurer will reclassify the treatment as maintenance. And your lien gets denied.

Resubmission won't fix it. The clinical record didn't support the claim in the first place.

How can my practice prepare for shifts in auto-insurance reimbursement and documentation rules?

Pull a sample of your PI cases from the last 12 months. Audit whether your clinical notes would survive the tighter medical necessity review that's coming in 2026.

Look for the gaps.

Visit notes that don't tie treatment to measurable functional improvement. Progress documentation that reads like maintenance care because the EHR auto-populates the same language every time. Treatment plans that extend past typical recovery timelines without objective markers justifying continued active care.

Then evaluate your billing partner.

Ask them how they handle multi-step appeals for PI liens under tighter documentation standards. Ask them what their process looks like when a claim requires a medical necessity argument that goes beyond resubmission.

If the answer is vague—or if they redirect the question back to you—you don't have a partner.

You have a submission service.

And submission services don't protect revenue when the rules change. They process claims until the system flags them as non-compliant, then move on.

Will the 2026 regulatory changes affect MedPay claims differently than third-party liability claims?

Yes. MedPay claims function as first-party coverage. The patient's own auto policy pays for medical expenses regardless of fault. That means faster adjudication and less friction because there's no liability dispute.

Third-party liability claims require establishing fault. Negotiating comparative negligence in contributory states. Waiting for the at-fault party's insurer to settle. The documentation scrutiny is higher because the insurer is contesting the claim, not just processing it.

So the 2026 changes hit third-party PI liens harder.

MedPay claims will still require tighter documentation under the new standards. But the adjudication timeline and payer cooperation are different.

The claims that take the longest and require the most human expertise to recover—the third-party liens—are the ones where the 2026 regulatory shift will expose whether your billing partner can argue medical necessity or whether they're just resubmitting the same documentation and hoping it clears.

What is the biggest financial risk for chiropractors when managing their own auto accident liens?

Aging AR that compounds silently while you assume the claim is being worked. The settlement timeline for a personal injury claim can stretch from a few months to over a year, and if your billing process doesn't proactively track lien priority, PIP exhaustion, and multi-step appeals, that revenue ages past the point of recovery.

For car accidents with minor to moderate injuries, personal injury settlements average between $15,000 and $30,000. And your lien sits inside that settlement pool alongside legal fees, other medical providers, and the patient's own recovery.

If your lien isn't filed correctly, if your documentation doesn't justify the full value of care, or if your billing partner doesn't negotiate lien reduction demands from the plaintiff's attorney, you recover a fraction of what you billed.

Or nothing at all.

And here's the part most practices don't realize until it's too late.

The volume-first billing model deprioritizes complex PI liens the moment they require more than two touches. The claim sits in your AR report while the biller focuses on the clean claims that clear fast. You never see the work stop. You just see the aging bucket grow.

That's the financial risk.

Not the claim getting denied. The claim getting abandoned while your practice assumes someone is working it.

What This Means for Your Practice

The 2026 regulations will change how PI liens get processed.

That's not the question.

The question is whether your current billing setup can handle that change—or whether it's built for a world that no longer exists.

Software platforms optimized for submission speed don't adapt to tighter documentation standards. They process what they're programmed to process. When the rules shift, the system flags the claim as non-compliant and moves on.

You're the one writing off the revenue.

Here's the split between a billing partner and a claim submission service.

A partner understands that the 2026 changes aren't just new codes—they're a fundamental shift in how insurers evaluate medical necessity for chiropractic PI claims.

A partner built for this knows how to document active care so it survives the new scrutiny. A partner with DC-founded vertical expertise knows what your charts need to say before the lien gets filed—not after the first denial comes back.

A volume-first billing company?

They'll treat this like a software update. Submit faster, process more, deprioritize the ones that don't clear in the first pass.

That model worked when PI liens were straightforward. It won't work under the 2026 framework—and the cost of that failure lands on your practice's AR, not theirs.

The real decision isn't whether you need help with PI billing.

You already know you do.

The decision is whether your current partner can protect your lien priority and argue medical necessity under the tighter standards—or whether they're running a throughput model that abandons complex claims the moment they require human judgment.

The 2026 regulations will answer that question for you.

Practices that wait for the answer will spend the next two years recovering from it. The ones who evaluate their billing partner now—before the new standards take effect—won't have to.

Bushido Billing LLC was built for exactly this kind of complexity. Not because we predicted the 2026 changes. Because we know what happens when a billing system encounters a scenario it wasn't programmed for.

Software can submit a claim. It cannot argue one.

Human expertise handles the appeals. Peer authority understands what your documentation needs to prove. And the performance-based model ensures we're incentivized to recover the revenue—not just submit the claim.

The 2026 regulations aren't a compliance update you can schedule around. They're a filter that separates billing partners who understand how to document chiropractic medical necessity from platforms that only know how to click Submit. A practice assessment shows you where your PI billing actually stands right now. How your documentation holds up under the tightened requirements. Whether your lien tracking protects revenue or just tracks it. What happens when a claim needs a human argument instead of another automated resubmission. Software can submit a claim. It can't argue one. Practices that assess their billing setup before the new standards hit won't spend 2026 recovering from claims that aged out while they assumed someone was working them. Schedule your practice assessment here.

© 2026 Bushido Billing. All Rights Reserved | Web Design by iTech Valet