How to Identify Bad PI Cases Before They Impact Your Clinic's Cash Flow?

A bad PI case looks recoverable at intake but structurally cannot generate cash flow. The attorney won't settle. Liability is disputed. Your documentation can't prove medical necessity. The patient stops treatment before the case builds value. These cases don't fail at settlement—they fail at acceptance, when your front desk says yes to a claim that was never going to pay.

Most clinics screen PI cases by verifying the patient has an attorney and an active claim. That's not vetting. That's hoping. The attorney's track record, the strength of liability evidence, the patient's compliance history, the documentation trail you'll need to defend your lien—those are the four revenue triage checkpoints that separate a recoverable case from aged accounts receivable that sits unpaid while your clinic finances someone else's legal gamble.

Over 95% of personal injury cases settle out of court. Your revenue recovery depends entirely on pre-litigation documentation quality and the attorney's willingness to prioritize your lien in settlement negotiations. The median settlement for car accident cases is around $20,000, but that figure is meaningless if your clinic's portion gets negotiated to zero because the case was accepted without vetting the attorney's communication style or the clarity of fault.

The timeline matters too. Simple claims can settle in a few months, but complex cases with severe injuries can stretch one to three years or more. That's one to three years of your clinic carrying the patient's balance on your books, aging past the point where accounts receivable over 120 days old drop to a collection rate below 10%. Every bad PI case you accept isn't just a lost opportunity. It's active financial bleeding that most billing companies won't tell you about until the case is already unrecoverable.

Last Updated: May 23, 2026

- The Real Cost of Accepting a Bad PI Case

- The 4-Point PI Case Vetting Framework

- Front Desk Screening Without Legal Advice

- What to Do When a Case Goes Bad Mid-Treatment

-

Frequently Asked Questions

- What is the single biggest red flag an attorney can show when discussing a new PI case?

- How can my front desk screen potential PI cases without giving legal or medical advice?

- Is it better to accept a PI case with a low-value insurance policy or no policy at all?

- What specific language should be in my clinic's PI lien agreement to protect our interests?

- If a PI case goes bad, what are the first steps to take to cut losses and protect cash flow?

- The Case You Don't Take Doesn't Hurt You

The Real Cost of Accepting a Bad PI Case

A bad PI case doesn't announce itself at intake. Patient has an attorney. Claim is active. Treatment plan looks reasonable. The red flags show up six months later when your AR report lists the case as unpaid, the attorney stops returning calls, and your biller tells you the lien is still in negotiation.

By then, the case has already cost you.

The real cost isn't the treatment you provided. It's the cash flow you didn't collect while carrying that balance. Every dollar tied up in a bad PI case is a dollar you can't use to pay staff, cover rent, or invest in equipment.

That's opportunity cost.

And it compounds every month the case sits unresolved.

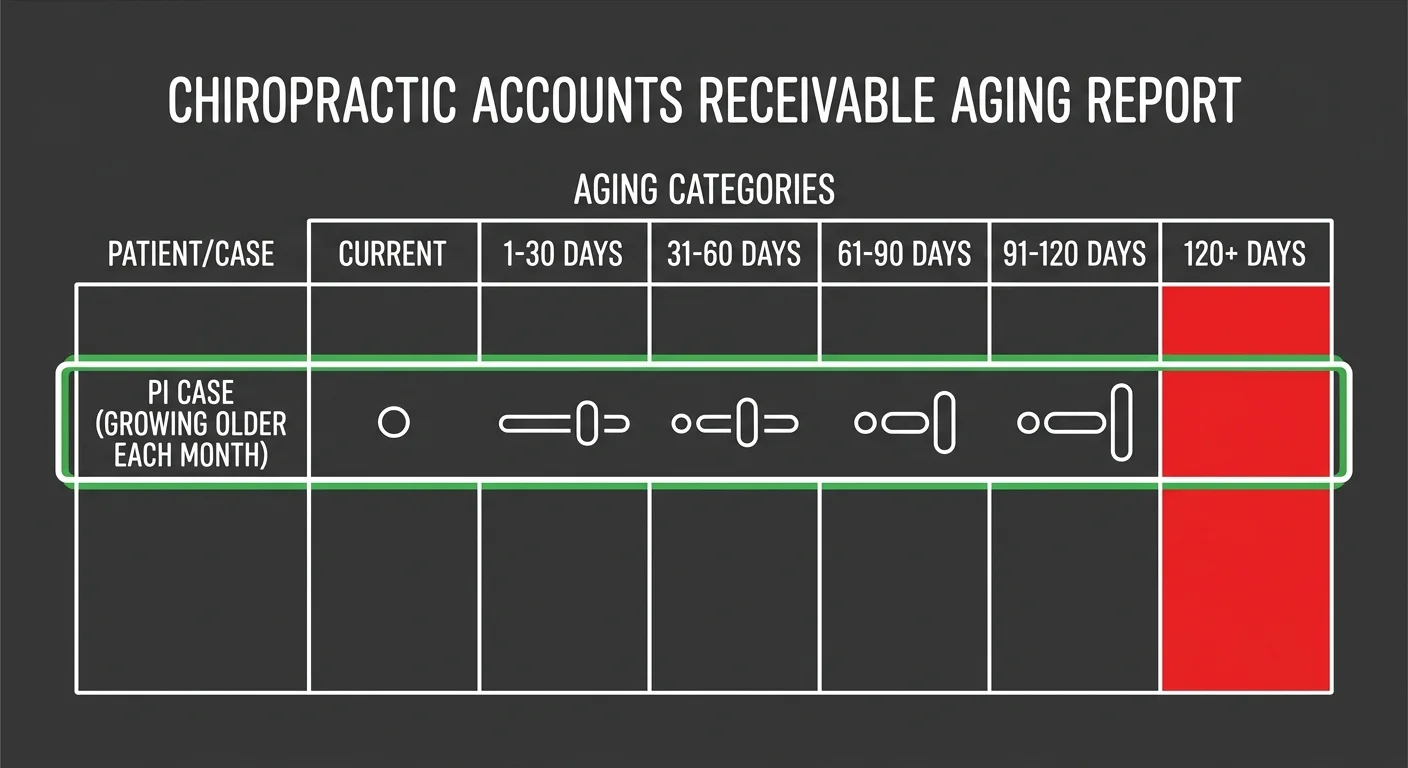

Here's the part most clinics don't calculate: accounts receivable over 120 days old drop to a collection rate below 10%.

Once a PI case crosses that threshold, you're not managing revenue recovery anymore. You're managing a write-off. The case isn't just unpaid—it's uncollectable. That's the difference between a denial you can appeal and a case that was never going to pay.

Why Insurance Verification Alone Fails

Most front desks verify insurance by confirming the patient has an attorney and an open claim.

That tells you the case exists.

It doesn't tell you whether the case will settle, whether the attorney prioritizes chiropractic liens, or whether the patient will complete enough treatment to justify your lien amount in negotiations.

Insurance verification answers the wrong question.

The question isn't 'Does this patient have a claim?' The question is 'Will this claim generate recoverable revenue for my clinic?' A claim can be active and well-documented and still result in zero payment if the attorney treats your lien as negotiable overhead.

Most billing companies don't vet cases at intake because their model isn't built for it. Volume-first billers optimize for submission speed, not recovery rate.

They accept every case that meets the minimum criteria because rejecting a case costs them potential revenue.

Your clinic absorbs the cost when those cases age into uncollectable AR.

What the Settlement Timeline Tells You

Simple claims can settle in a few months, but complex cases with severe injuries can stretch one to three years or more.

That timeline is the most important number your front desk never asks about. It determines how long your clinic finances the patient's legal case—and whether your cash flow can survive the wait.

The median settlement for car accident cases is around $20,000, but that figure is meaningless without context.

If the case takes two years to settle and your lien is $8,000, you've carried $8,000 in unpaid AR for 24 months. That slot in your patient schedule could have been filled by an insurance case that pays within 30 days.

Every PI case you accept is a bet on your clinic's cash flow survival. If the case settles quickly and your lien is prioritized, you win. If the case drags past 120 days and the attorney deprioritizes your lien in negotiations, you lose.

And the loss isn't just the unpaid balance. It's every other case you didn't take because that treatment slot was occupied.

What Policy Limits Actually Mean

Policy limits are the upper boundary of what the insurance carrier will pay for the entire claim—not just your clinic's portion.

If the at-fault driver has a $25,000 policy limit and the patient's total medical bills exceed that amount, every provider with a lien is competing for the same limited pool of settlement funds.

And the attorney decides how those funds get allocated.

Your lien doesn't automatically receive full payment just because you provided documented care. The attorney negotiates lien reductions to maximize the client's net settlement. Chiropractic liens are the first target for reduction—they're perceived as easier to negotiate down than hospital or surgical liens.

So when your front desk asks 'Does the patient have insurance?' they're asking the wrong question.

The right question is 'What are the policy limits, and how many other providers have liens on this case?' That tells you whether there's enough settlement value to cover your lien—or whether you're accepting a case that's already financially exhausted before your clinic even starts treatment.

Understanding factors that impact settlement value is the first step in vetting cases that won't bleed your cash flow dry.

| Settlement Timeline | Typical Duration | Cash Flow Impact |

|---|---|---|

| Simple Claim (Clear Liability) | A few months | Minimal AR aging — cash flow recovers within standard billing cycle |

| Complex Case (Disputed Liability or Severe Injury) | 1–3 years or more | Clinic finances patient balance for years — treatment slot occupied by unpaid case while similar slots generate monthly insurance revenue |

| Case Exceeding 120 Days | 4+ months without settlement | Collection rate drops below 10% — case transitions from revenue recovery to write-off territory |

| Median Settlement Case | Variable (depends on liability and documentation) | Median settlement of $20,000 must cover all provider liens, patient net, and attorney fees — your lien competes for limited funds |

The 4-Point PI Case Vetting Framework

A vetting framework your front desk can't execute is a bottleneck, not a system.

The four checkpoints below are behavioral screens—observable, documentable, and predictive of whether a case generates recoverable revenue or ages into uncollectable AR.

These four checkpoints filter for specific failure modes.

Attorney Quality screens out lawyers who deprioritize chiropractic liens. Liability Clarity screens out disputed-fault cases that stall settlements. Documentation Strength screens out cases that won't survive a medical necessity challenge. Patient Compliance Indicators screen out patients who won't complete enough treatment to justify your lien.

Every case that passes all four has a documented path to recovery.

Attorney Quality

The attorney is the single most important variable in your revenue recovery.

They control settlement negotiations. They control lien prioritization. They control communication timelines.

A high-volume personal injury attorney who treats chiropractic liens as negotiable overhead will deprioritize your clinic every time. Why? Reducing your lien increases their client's net settlement—and their contingency fee.

Your front desk should ask three questions during intake.

Does the attorney specialize in personal injury? How many chiropractic cases have they handled in the past year? Do they communicate proactively with providers, or does your clinic chase them for updates?

These questions reveal whether the attorney views your clinic as a partner or a cost center.

And here's the screening question most clinics never ask: Has this attorney ever reduced or negotiated down a chiropractic lien without the clinic's consent?

If the answer is yes—or if the patient doesn't know—that's a red flag.

That attorney has already demonstrated they'll sacrifice your revenue to close a settlement faster. Understanding common attorney objections to PI settlements gives you the language to screen for these patterns before the case enters your schedule.

Liability Clarity

Clear liability means fault is undisputed. Rear-end collisions, red-light violations, left-turn accidents with police reports—high-clarity cases.

Disputed liability means multiple parties share fault, or the at-fault driver contests responsibility.

Disputed cases take longer to settle. And settlement offers get reduced to account for the risk of losing at trial.

Your front desk should verify that a police report exists and that the at-fault driver was cited or clearly identified as responsible.

If the patient says "the other driver's insurance is investigating" or "we're still figuring out who was at fault," that case is already high-risk.

Insurance carriers investigating liability are hunting for reasons to deny or reduce the claim. And your clinic's lien is tied to the outcome.

The statute of limitations adds another layer of urgency.

Most states allow between one to six years to file a lawsuit. Once the deadline passes, the case is legally dead.

If the patient walks in 18 months after the accident and your state has a two-year statute, you have six months of runway before the attorney must file or settle. That's not enough time to complete a treatment plan and build lien value. Decline the case at intake.

Documentation Strength

Over 95% of personal injury cases settle out of court.

That means your lien's value is determined entirely by the documentation you produce before the settlement is finalized. If your notes can't prove every visit was medically necessary and causally linked to the accident, the attorney will reduce your lien during negotiations.

Or the opposing insurance carrier will demand it as a condition of settlement.

A significant percentage of claim denials or reductions in PI cases stem from insufficient proof of medical necessity or a disputed causal link between the accident and the treatment.

That means your clinical documentation must answer two questions every time: Why was this visit necessary? How does this visit directly relate to the injuries caused by the accident?

If your notes don't answer both questions clearly, the lien is vulnerable.

So your front desk should ask whether the patient has seen any other providers since the accident. Chiropractors, physical therapists, urgent care, emergency rooms.

If the patient has a fragmented treatment history across multiple providers, your clinic's lien competes with every other provider's lien for the same settlement pool. And if there are gaps in treatment—weeks or months where the patient received no care—those gaps weaken the causal link and make your lien easier to dispute.

Strong medical necessity documentation is the only defense against these challenges.

Patient Compliance Indicators

Compliance isn't about whether the patient is polite.

It's about whether the patient will complete the treatment plan.

A patient who misses appointments, cancels frequently, or stops treatment after two visits doesn't generate enough lien value to justify your clinic's time and cash flow investment. And if the patient stops treatment before the case settles, you're left carrying a low-value lien the attorney will deprioritize in negotiations.

Your front desk should verify the patient's work schedule, transportation situation, and childcare constraints before accepting the case.

If the patient works two jobs with no flexible hours, has no reliable transportation, and has three kids under five, the likelihood of consistent twice-weekly treatment is low.

That's not a judgment about the patient's character. It's a realistic assessment of whether the case can build enough lien value to recover revenue.

And here's the question most clinics never ask: Has this patient completed a course of chiropractic treatment in the past?

If the answer is no, you're betting on compliance with no track record to validate that bet. If the answer is yes, ask how many visits they completed—and whether they finished the care plan or stopped mid-treatment.

That history predicts future behavior.

A patient with a history of incomplete treatment is a bad PI case waiting to happen. And your clinic's cash flow can't afford to find out after the patient ghosts you at visit six. Specialized Personal Injury (PI) Lien Billing requires the discipline to walk away from cases that don't meet all four checkpoints—because every case you decline protects the cash flow generated by the cases you accept.

| Vetting Checkpoint | Green Flag | Red Flag | Why It Matters |

|---|---|---|---|

| Attorney Quality | PI specialist with documented history of protecting chiropractic liens; proactive communication; transparent lien negotiation process | High-volume generalist attorney; no chiropractic case history; has reduced provider liens without consent; clinic must chase for updates | The attorney controls settlement negotiations and lien prioritization. An attorney who views your lien as negotiable overhead will sacrifice your revenue to maximize their contingency fee. |

| Liability Clarity | Undisputed fault with police report; at-fault driver cited; rear-end collision or clear traffic violation; insurance accepted liability | Disputed fault between multiple parties; no police report or unclear responsibility; insurance carrier still investigating; patient unsure who was at fault | Disputed liability cases take longer to settle and produce reduced settlement offers. Your lien is tied to the outcome, and delayed settlements age into uncollectable accounts receivable. |

| Documentation Strength | Clear accident mechanism; single provider or coordinated treatment; no treatment gaps; patient has documented injury consistent with accident type | Fragmented treatment across multiple providers; weeks or months with no care; vague injury description; patient treated elsewhere before your clinic; pre-existing conditions not documented | Settlement negotiations hinge on proving medical necessity and causal link. Fragmented care and treatment gaps weaken your lien and make it the first target for reduction during attorney negotiations. |

| Patient Compliance Indicators | Stable work schedule with flexible hours; reliable transportation; history of completing prior chiropractic treatment plans; clear understanding of lien billing process | Works multiple jobs with no schedule flexibility; no reliable transportation; childcare constraints; no history of completing treatment; missed or canceled first appointment | A patient who stops treatment after a handful of visits doesn't generate enough lien value to justify your cash flow investment. Incomplete treatment leaves you carrying a low-value lien the attorney will deprioritize. |

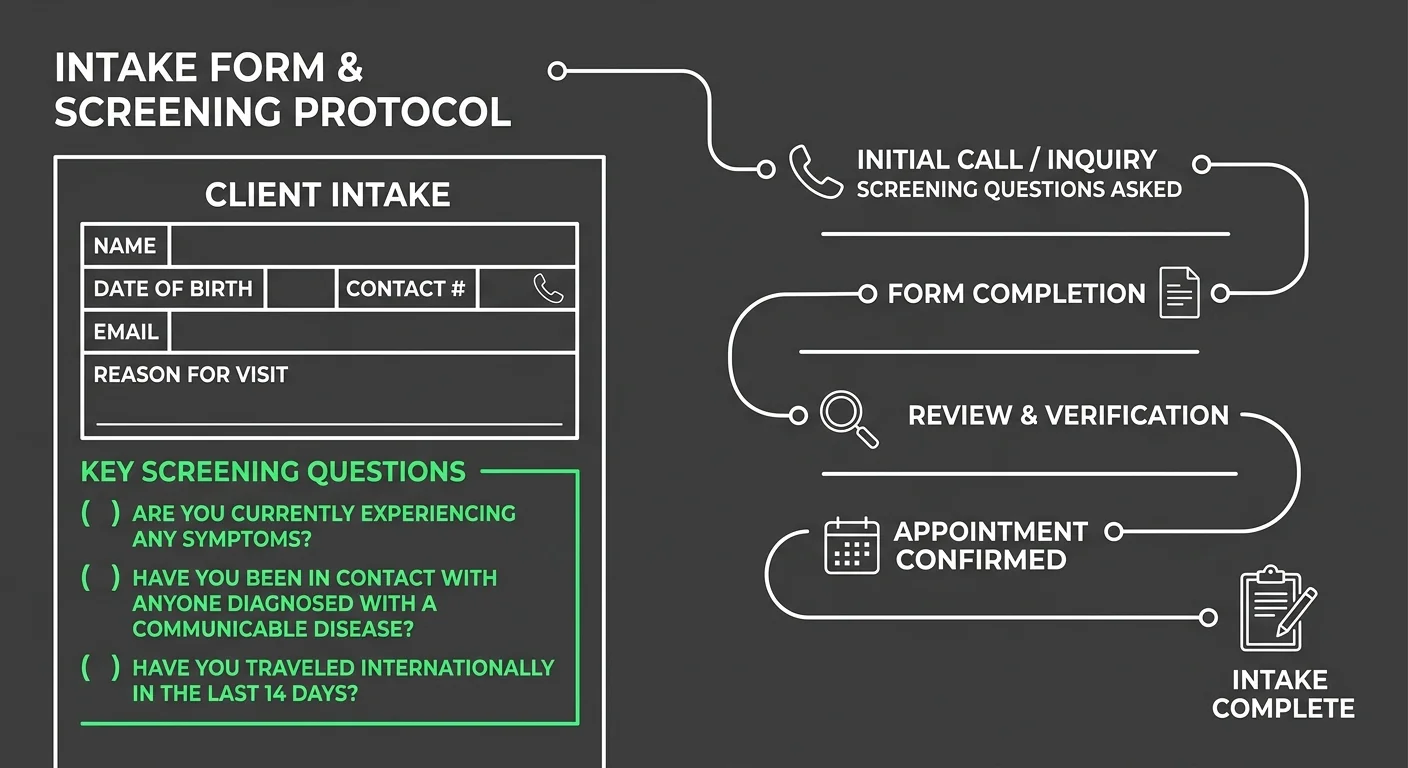

Front Desk Screening Without Legal Advice

A vetting framework that only your billing manager can execute is a bottleneck, not a system.

The patient calls your front desk. Not your back office.

By the time your billing team reviews the case, you've already scheduled the first three visits and committed staff hours to a patient who may never generate recoverable revenue.

Your front desk needs a script that filters cases without requiring legal interpretation, medical judgment, or diagnostic expertise. That script collects objective, documentable data points that reveal whether a case has a clear path to settlement.

Or whether it's going to become aged accounts receivable that sits unworked because the attorney stopped returning calls and the settlement timeline stretched past the two-year mark.

The questions below are behavioral screens.

They don't ask your front desk to evaluate fault or diagnose injury severity. They ask the patient to confirm facts that predict cash flow outcomes. Every question maps to one of the four checkpoints defined earlier.

Every answer either clears the case for intake or triggers an escalation to your billing specialist before the patient is scheduled.

What to Ask Before Committing

Start with the attorney's name and contact information. Then ask: How long have you been working with this attorney?

If the patient retained the attorney within the past 30 days and the accident happened six months ago, that's a red flag. The patient has already been turned down by other attorneys, or the case sat unrepresented for months while the statute of limitations burned down.

Next, ask whether the attorney has sent a letter of representation to the at-fault driver's insurance carrier.

If the answer is no, the case isn't officially active. The insurance carrier has no legal obligation to preserve settlement funds. Other providers can file liens ahead of your clinic.

By the time your lien is recorded, the settlement pool is already allocated.

Then ask whether the patient has already started treatment with another chiropractor, physical therapist, or medical provider for this accident. If yes, ask why they're switching providers.

'My last chiropractor wouldn't take a lien' is a green flag. It means the patient is committed to treatment and understands the lien model.

'My last chiropractor said the case wasn't worth it' is a red flag. It means another clinic already vetted this case and walked away.

And here's the question that separates high-value cases from cash flow traps: What is the at-fault driver's insurance policy limit?

If the patient doesn't know, ask whether the attorney has confirmed coverage. If the attorney hasn't confirmed coverage yet, the case is speculative. You're betting your clinic's cash flow on the assumption that the at-fault driver carries enough insurance to cover your lien, the patient's medical bills, the attorney's fee, and the patient's net settlement.

That's not vetting. That's gambling.

Understanding negotiating attorney liens requires knowing the settlement ceiling before you accept the case—because once you've provided care, you've already committed your clinic's resources to a case that may have no recoverable value.

When to Escalate to a Billing Specialist

But some cases require expertise your front desk doesn't have.

If any of the following situations come up during intake, escalate the call to a dedicated biller or billing manager before scheduling the patient.

- The patient mentions that multiple vehicles were involved in the accident, or fault is still being determined by the insurance carrier

- The accident happened more than 12 months ago and the patient has not yet started treatment

- The patient has already seen three or more providers since the accident and is now looking for a fourth

- The attorney is a general practice lawyer who does not specialize in personal injury

- The patient cannot provide the attorney's contact information or says 'my attorney will call you later'

These escalation triggers don't mean the case is automatically declined.

They mean the case requires a second layer of vetting that accounts for variables your front desk script can't capture. Prior lien volume. Fragmented treatment history. Attorney relationships your billing team already knows are bad.

A front desk that escalates appropriately protects your clinic's cash flow without turning away cases a billing specialist could still approve. A front desk that schedules every case without escalation turns your intake process into a cash flow risk generator.

By the time your billing team spots the problem, you've already invested weeks of care into a case that was never going to pay.

| Question Category | Example Phrasing | What You're Really Screening For |

|---|---|---|

| Attorney Quality | How long have you been working with this attorney? | Whether the patient retained counsel immediately after the accident or whether the case sat unrepresented for months—suggesting other attorneys declined it |

| Attorney Quality | Has your attorney sent a letter of representation to the at-fault driver's insurance carrier? | Whether the case is officially active—if no letter has been sent, other providers can file liens ahead of yours and the settlement pool may already be allocated |

| Liability Clarity | Were multiple vehicles involved in the accident? | Whether fault is clear or whether the case involves comparative negligence disputes that delay settlement and reduce recoverable amounts |

| Liability Clarity | What is the at-fault driver's insurance policy limit? | Whether the settlement ceiling is high enough to cover your lien, other providers' liens, attorney fees, and the patient's net settlement—or whether you're gambling on insufficient coverage |

| Documentation Strength | Have you seen any other providers since the accident? | Whether your lien competes with multiple other providers for the same settlement pool—and whether fragmented treatment history weakens the causal link between the accident and your care |

| Documentation Strength | When did the accident happen, and when did you start treatment? | Whether there are treatment gaps that insurance carriers and attorneys will use to dispute medical necessity—gaps weaken your lien's defensibility in negotiations |

| Patient Compliance Indicators | What is your work schedule like, and do you have reliable transportation? | Whether the patient can realistically commit to twice-weekly treatment over several months—a patient with no flexible hours and no transportation won't build enough lien value to justify your cash flow investment |

| Patient Compliance Indicators | Have you completed a course of chiropractic treatment in the past? | Whether the patient has a track record of following through on care plans—or whether they have a history of stopping mid-treatment, which predicts they'll ghost your clinic before the lien builds recoverable value |

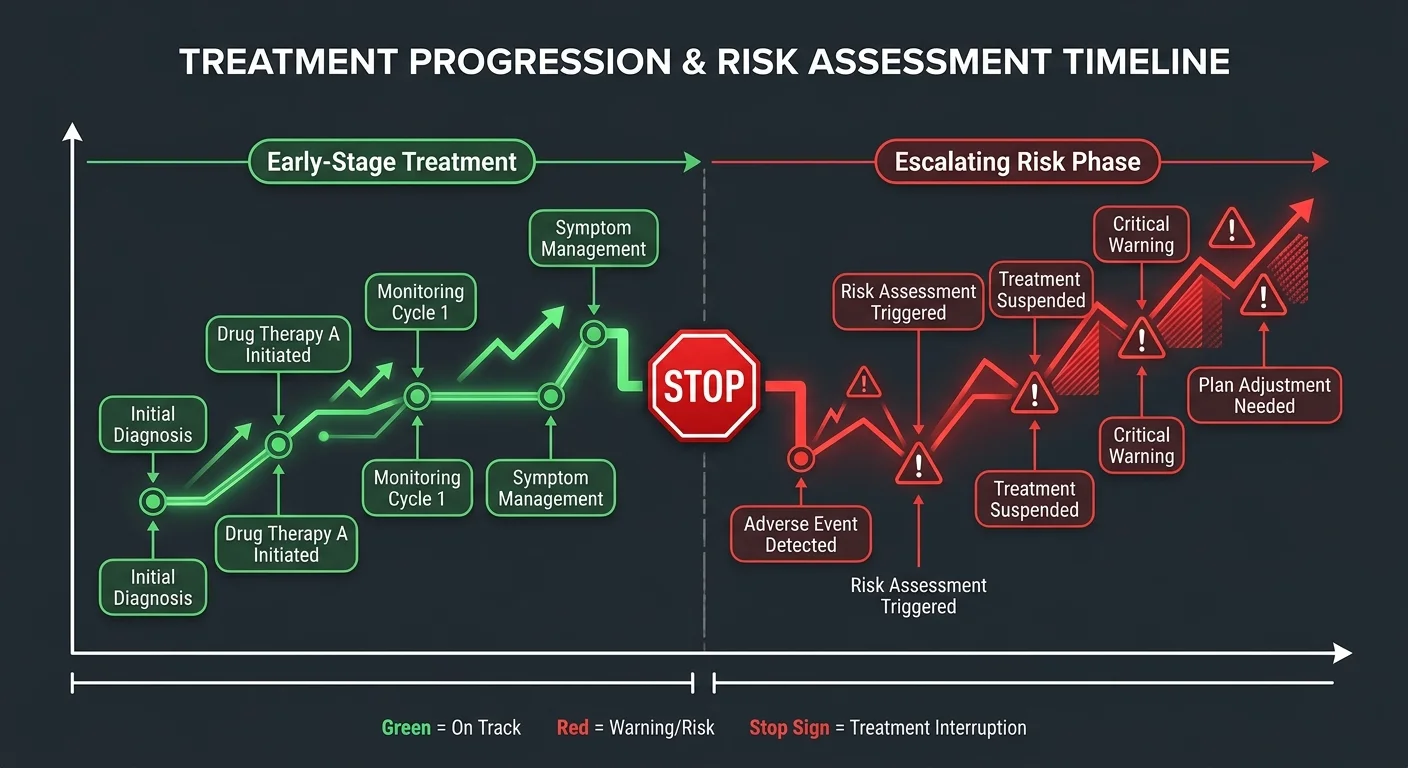

What to Do When a Case Goes Bad Mid-Treatment

Not every bad case announces itself at intake.

Some collapse weeks or months in. The attorney stops returning calls. The patient misses three appointments in a row. The insurance carrier disputes liability mid-claim.

By the time you realize the case is going bad, you've already provided care, documented visits, and carried the lien on your accounts receivable.

Your clinic's cash flow is exposed.

And the longer you wait to act, the worse the exposure gets.

You need a mid-stream escape protocol. A decision tree that tells you when to protect your lien, when to stop treating, and when to cut losses before a recoverable case turns into aged AR no one will work.

Complex cases with severe injuries can take 1-3 years or more to settle. A case that looks fine at month two can become a cash flow trap by month eight if you miss the warning signs.

Clinics that protect cash flow triage bad cases mid-treatment with the same discipline they use at intake.

How to Protect Your Lien

The moment a case shows red flags — patient compliance drops, attorney goes silent, opposing carrier disputes liability — you document every remaining visit with maximum specificity.

Your SOAP notes for every subsequent visit must justify medical necessity. Tie every adjustment to the accident-related diagnosis. Demonstrate objective improvement or lack of improvement that supports continued care.

If the case goes to dispute or if the lien is challenged during settlement negotiations, your documentation is the only evidence that your care was reasonable and necessary.

And you send a written status update to the patient's attorney immediately.

Not an email asking for an update. A letter that documents the patient's current treatment status, the number of visits completed, the anticipated discharge date, and the current lien balance.

This letter serves two purposes. It reminds the attorney that your lien exists and is growing. And it creates a paper trail showing you attempted to communicate proactively while the case was still active.

If the attorney doesn't respond within 10 business days, send a follow-up. If the attorney still doesn't respond, that's a clear signal the case is no longer a priority for them.

Which means it shouldn't be a priority for your clinic either.

So you escalate internally to your billing team or a DC-founded billing partner who specializes in PI lien recovery.

They review the case to determine whether the lien is still defensible, whether the attorney relationship is salvageable, and whether continuing treatment increases your recoverable lien value or simply increases your exposure.

Accounts receivable over 120 days old have a collection rate that can drop below 10%. Every additional visit you provide to a deteriorating case is a bet against your own cash flow.

Protecting your lien means knowing when to stop growing it.

When to Stop Treating

Here's the hard truth: some cases are worth more to your clinic if you discharge the patient early and file a smaller lien than if you continue treatment and carry a larger lien that never pays.

A $3,000 lien that settles within six months is better for your cash flow than a $12,000 lien that ages past 18 months and becomes uncollectable.

The question isn't whether the patient still needs care.

It's whether the case can still generate recoverable revenue.

You stop treating when the case meets any of these triggers: attorney stops responding after two documented attempts, patient misses three consecutive scheduled visits without rescheduling, insurance carrier formally denies liability and the attorney isn't pursuing dispute, or your billing team determines the lien is no longer defensible.

None of these triggers mean you abandon the patient clinically.

They mean you transition the patient from lien-based care to a different payment model. Cash pay. Health insurance if they have it. Or a documented hardship discharge if neither option is viable.

What you can't do is continue providing care on a lien your own billing team has already determined won't recover. That's not patient care. That's cash flow self-sabotage.

Understanding how to maximize personal injury (PI) lien recovery includes knowing when not to chase recovery at all. Every hour your clinic spends working a dead case is an hour you're not spending on cases that will actually pay.

| Warning Sign | Immediate Action | Why This Protects Cash Flow |

|---|---|---|

| Patient misses three consecutive appointments without rescheduling | Document the missed appointments in the patient chart and send a written status update to the attorney noting treatment disruption and current lien balance | Creates a paper trail showing non-compliance before the lien grows further, protecting your ability to justify discharge if the case never settles |

| Attorney stops returning calls or emails for more than 10 business days | Send a certified letter documenting treatment status, anticipated discharge date, and current lien amount—then escalate to your billing team for case review | Proves proactive communication and signals internally that the case may no longer be a priority for the attorney, allowing you to stop treatment before AR ages further |

| Opposing insurance carrier formally disputes liability mid-treatment | Confirm with the attorney whether they are pursuing litigation; if not, transition the patient to a cash-pay or health insurance payment model immediately | Prevents your clinic from continuing lien-based care on a case with no clear path to settlement, cutting exposure before the lien becomes uncollectable AR |

| Patient discloses they are switching attorneys or considering dropping the case | Stop scheduling future appointments and notify your billing team immediately to assess whether the existing lien is still defensible | A case in transition is a case without representation, which means no one is advocating for your lien—continuing care at this stage increases exposure with no recovery path |

| Attorney confirms policy limit is insufficient to cover all recorded liens | Calculate your clinic's lien priority and compare it to the total lien pool—if your lien will be reduced to zero or near-zero, discharge the patient and file the lien as-is | A smaller lien filed early is better for cash flow than a larger lien that grows while other providers exhaust the settlement pool, leaving your clinic with aged AR and no recovery |

| Patient requests a lien reduction or asks to negotiate payment terms mid-treatment | Do not negotiate lien terms with the patient directly—escalate to your billing specialist and attorney to determine whether the request signals financial pressure or settlement negotiation | Lien reduction requests often indicate the patient knows the settlement is small or that the attorney is preparing to challenge provider liens, giving you early warning to protect your position |

| Documentation review reveals gaps in medical necessity or lack of objective improvement | Strengthen documentation immediately for all future visits and consider discharging the patient if continued care cannot be justified with clinical evidence | Weak documentation makes your lien indefensible during settlement negotiations, meaning every additional visit on a poorly documented case increases your uncollectable AR rather than your recoverable lien |

Frequently Asked Questions

The framework is built. The four checkpoints are locked in. The escalation triggers are documented.

But knowing the system isn't the same as using it.

What follows are the five questions clinics ask when they're trying to vet PI cases without second-guessing every intake decision.

These aren't theoretical.

They're the objections that stop front desks from screening. The edge cases that stop billing teams from escalating bad cases mid-treatment. The doubts that stop practice owners from saying no when they should.

The answers are direct. And they assume you'd rather protect your cash flow than hope a bad case fixes itself.

What is the single biggest red flag an attorney can show when discussing a new PI case?

The attorney doesn't specialize in personal injury.

That's the clearest signal the case will take longer, settle for less, and require more hand-holding than your billing team has capacity for.

A general practice attorney handling a PI case as a favor doesn't have the negotiation power, the insurance adjuster relationships, or the litigation threat credibility that moves settlements forward. They're learning on your lien's timeline. Every month they spend figuring out the process is a month your accounts receivable ages without progress.

If the attorney's website lists family law, estate planning, and personal injury all on the same page, escalate the case to your billing team before scheduling the patient.

That's not snobbery.

That's cash flow protection.

How can my front desk screen potential PI cases without giving legal or medical advice?

Your front desk asks four factual questions and escalates based on the answers.

Question one: Who is your attorney? If the patient doesn't have one yet, escalate.

Question two: What's the name of the at-fault driver's insurance company? If the patient doesn't know, escalate.

Question three: Have you seen any other providers for this injury since the accident? If yes and they're now coming to you, escalate.

Question four: Can you provide your attorney's contact information so we can send them our lien agreement? If the patient says the attorney will call later, escalate.

None of these questions require your staff to give legal or medical advice. They're intake facts that determine whether the case meets baseline recoverability criteria or whether a billing specialist needs to vet it further.

A front desk that asks these four questions protects your cash flow without overstepping scope of practice.

A front desk that skips them schedules every case as if they're all equal.

And they're not.

Is it better to accept a PI case with a low-value insurance policy or no policy at all?

No policy at all is better than a low-value policy that's already exhausted by other providers' liens.

Here's why.

If the at-fault driver has no insurance, the case is unambiguously unworkable and you decline it immediately. If the at-fault driver has a $15,000 policy and there are already two providers with recorded liens totaling $18,000, your clinic is fighting for scraps from a settlement pool that doesn't exist.

The median settlement for personal injury cases involving car accidents is around $20,000. Once you account for the attorney's contingency fee and the other providers' liens, a low-value policy turns into a race to file your lien first—not the same thing as getting paid.

So ask the attorney for the policy limit disclosure before you accept the case.

If they won't provide it, that tells you everything you need to know about whether they view your lien as recoverable.

Speculation is not a revenue model.

What specific language should be in my clinic's PI lien agreement to protect our interests?

Your lien agreement must include three specific clauses.

Clause one: the patient authorizes the attorney to pay your clinic directly from the settlement proceeds before disbursing any funds to the patient.

Clause two: the patient agrees that the lien survives the termination of the attorney-client relationship. If the patient fires their attorney mid-case, your lien doesn't disappear.

Clause three: the patient acknowledges that if the settlement is insufficient to cover all recorded liens, your clinic reserves the right to pursue collection directly from the patient.

These three clauses don't guarantee you'll get paid.

They guarantee you have legal standing to pursue payment if the case goes sideways.

A lien agreement without those clauses is a courtesy letter, not a contract. And courtesy doesn't protect cash flow when a case collapses six months into treatment.

Your attorney can review your clinic's lien template to confirm it includes enforceable language. But these three clauses are the baseline for any PI case your clinic accepts on a lien basis.

If a PI case goes bad, what are the first steps to take to cut losses and protect cash flow?

Stop providing care on the lien immediately. Send written notice to the attorney within 48 hours.

That notice states the patient's current lien balance, the number of visits completed, the reason you're discontinuing lien-based care, and the deadline by which the attorney must respond if they want to discuss a resolution.

Each state has a strict statute of limitations for filing a personal injury lawsuit, typically ranging from one to six years from the date of the injury. If the case is approaching that deadline without a settlement or litigation filed, your lien is at risk of expiring entirely. The written notice creates a paper trail showing you attempted to protect your lien while the case was still salvageable.

Then you escalate to a billing partner who handles PI lien recovery.

The next steps—filing a lien with the court, negotiating a reduced settlement to accelerate payment, or transitioning the patient to a different payment model—require expertise your front desk doesn't have.

Accounts receivable over 120 days old have a collection rate that can drop below 10%. Every day you wait hoping the case fixes itself is a day your recoverable revenue becomes unrecoverable.

Cut losses fast. Protect the lien you've already earned.

And understand that stopping treatment early is sometimes the only way to get paid at all.

The Case You Don't Take Doesn't Hurt You

The case you don't take doesn't hurt you.

It doesn't land in your AR aging report. It doesn't occupy a treatment slot while the patient ghosts after three visits. It doesn't burn your biller's time chasing an attorney who won't answer calls.

And it doesn't quietly bleed your cash flow for eighteen months while you assume someone's working it.

Every bad PI case you decline at intake is a bullet your clinic didn't have to dodge later. The discipline to say no is worth more to your cash flow than the optimism to say yes to everything that walks through your door.

The triage framework you built—Attorney Quality, Liability Clarity, Documentation Strength, Patient Compliance Indicators—exists to protect your clinic from cases that were never going to pay.

Not because the patient didn't need care.

Not because the attorney's incompetent.

But because the case structure itself makes revenue recovery speculative. And speculation isn't a business model.

Volume-first billers ignore this reality because their model is built on submission speed, not recovery outcomes. They accept every case because they're not the ones carrying the risk.

You are.

The moment you accept a bad case, you've committed your clinic's resources to a lien that may never convert. That's the cost of saying yes without revenue triage.

So the next time a PI case walks into your clinic, ask yourself: does this case pass all four checkpoints, or are you accepting it because you're hoping the problems resolve themselves later?

Hope is not a vetting strategy.

Revenue triage is.

The clinics that protect their cash flow are the ones that say no early, say no often, and understand that the case you decline today is the cash flow crisis you avoided six months from now.

That's not pessimism.

That's triage.

And triage is the only reason some clinics survive PI billing while others drown in aged accounts receivable they assumed would eventually pay.

The four-checkpoint framework protects your clinic from bad cases. But revenue triage only works if someone's actually executing it—every intake call, every mid-stream warning sign, every lien negotiation that goes sideways. The clinics that survive PI lien billing don't just screen better. They work with a DC-founded billing partner who understands what case vetting costs when you get it wrong—and who handles specialized Personal Injury (PI) Lien Billing so your front desk isn't the last line of defense between a bad case and your clinic's cash flow.

© 2026 Bushido Billing. All Rights Reserved | Web Design by iTech Valet