How to Use PI Lien Revenue to Fund Your Practice Expansion?

Personal injury lien revenue funds practice expansion by converting outstanding PI claims into immediate working capital through accounts receivable financing or medical lien funding arrangements. Your PI liens are locked capital. You've already earned the revenue. But you won't see it for months or years while legal cases move forward.

Financing companies purchase these liens at a discount in exchange for cash now. You get the funds immediately instead of waiting through the full legal timeline. That capital covers the upfront expansion costs: new equipment, leasehold improvements, additional staff.

The financing is typically structured as a non-recourse advance. If the legal case fails, you don't repay the funds. The financing company assumes the collection risk. Your practice receives predictable capital based on the projected value of your PI lien portfolio. The lender collects directly from the settlement when the case resolves.

Successful execution requires three conditions.

First, your PI liens must be accurately valued and properly documented. Financing companies assess risk based on case strength, attorney quality, and your historical recovery rates.

Second, your practice needs a detailed business plan that demonstrates how the capital will generate returns that justify the discount rate.

Third, you need a billing partner who can prove your PI liens are being worked strategically, not passively aging in a spreadsheet.

This isn't for practices treating PI cases as incidental revenue. It's a strategic capital tool for practices with consistent PI volume, strong attorney relationships, and the operational infrastructure to turn complex claims into predictable capital.

Last Updated: May 23, 2026

- Why Most Practices Can't Turn PI Liens Into Growth Capital

- What Makes PI Lien Revenue Predictable Enough to Fund Expansion

- How PI Lien Financing Actually Works

- Structuring Your Expansion Plan Around PI Revenue

- The Role of a Specialized Billing Partner in Making This Work

-

Frequently Asked Questions

- How does funding from PI liens differ from a traditional small business loan?

- What percentage of a PI lien's face value can a practice typically secure as upfront capital?

- What are the primary risks of using future PI revenue to fund current expansion projects?

- How does a partnership with a specialized billing company impact the ability to secure financing against PI liens?

- What documentation is required to prove the value of outstanding PI liens to a lender or financing company?

- Where This Leaves You

Why Most Practices Can't Turn PI Liens Into Growth Capital

Here's the problem.

Most practices treat PI liens like difficult accounts receivable. Something to collect eventually. When the attorney calls. When the case settles. Whenever that happens.

That's why PI revenue stays locked.

Financing companies don't advance capital against hope. They advance against predictable, defensible revenue streams.

If your practice can't show that your PI liens are being actively worked — documented, tracked, escalated through a structured process — those liens have no financing value.

They're aging AR with legal complications attached.

The Gap Between Passive Collection and Strategic Capital

The financing gap isn't about the quality of your clinical work.

It's about documentation and execution. Financing companies assess risk by reviewing your historical recovery rates, your case tracking systems, and the average time from treatment to payment.

Most practices don't track that data.

They don't keep case-level documentation of treatment plans, lien filings, or settlement negotiation timelines. When a financing company asks for proof that your PI portfolio is worth advancing against, the practice has anecdotes. Not evidence.

This is where passive collection and strategic capital split.

Personal Injury (PI) lien billing isn't just about getting paid. It's about creating the operational infrastructure that turns delayed revenue into immediate, usable capital. Without that infrastructure, your PI liens stay locked no matter how strong the underlying cases are.

What Makes PI Lien Revenue Predictable Enough to Fund Expansion

Predictability is the difference between locked capital and leverageable capital.

Financing companies don't advance funds against optimistic projections. They don't advance against strong attorney relationships alone.

They advance against documented proof.

Your PI liens convert at predictable rates. Within predictable timeframes. With predictable risk profiles.

Most practices don't have that proof.

They track PI revenue as problem AR that eventually resolves itself. Not as a strategic asset.

Documentation That Proves Value

Financing companies assess value using three data points.

Historical recovery rates. Average time from treatment to settlement. Case-level documentation that shows active management.

If you can't produce those metrics on demand, your PI portfolio has no financing value. No matter how much revenue sits in it.

Every PI case in your portfolio needs a complete documentation trail.

Treatment dates. Lien filing confirmations. Attorney contact logs. Settlement negotiation timelines. Case status updates.

That documentation proves the lien isn't just aging. It's moving through a structured process with measurable milestones.

But here's what breaks most practices.

They assume the attorney's office tracks all of this. The attorney isn't tracking your revenue. The attorney tracks the legal case.

The gap between those two timelines is where your capital stays locked.

A specialized billing partner closes that gap by maintaining parallel documentation that ties clinical treatment to legal milestones. When a financing company asks for proof of value, you have it.

Case Selection and Attorney Relationship Standards

Not every PI case is worth financing against.

Cases with weak liability, uncooperative patients, or attorneys who don't communicate create unpredictable outcomes. Financing companies discount those cases heavily. Or exclude them.

The practices that maximize personal injury (PI) lien recovery consistently don't take every PI case that walks through the door.

They pre-qualify based on case strength, attorney reputation, and patient compliance. That selectivity creates a portfolio with higher predictability.

Higher predictability translates into better financing terms.

Your attorney relationships signal risk.

If you work with attorneys who settle cases quickly, communicate proactively, and protect provider liens during negotiations, your portfolio is predictable.

If you work with attorneys who go silent for months or deprioritize medical liens during settlement discussions, your portfolio is speculative.

Financing companies know the difference.

Proactive Communication as a Value Signal

Here's the thing.

Financing companies don't just evaluate your historical recovery rates. They evaluate whether you'll know if a case is deteriorating before it's too late to act.

That requires real-time visibility. Not quarterly check-ins with the attorney's office.

A billing partner who can track PI case progress without burning attorney relationships is a financing asset.

Weekly updates. Proactive case status inquiries. Escalation protocols for stalled cases.

These prove you're not waiting passively for settlement checks. You're managing PI revenue as a strategic operation.

And that makes it predictable enough to fund expansion.

| Documentation Type | What It Proves | Why Lenders Require It |

|---|---|---|

| Treatment dates and clinical notes | The lien is tied to documented care, not speculative future services | Confirms the revenue exists and is anchored to verifiable treatment |

| Lien filing confirmations and legal acknowledgments | The attorney and patient are aware of the provider's secured interest | Protects the lender's position in the event of settlement |

| Attorney contact logs and case status updates | The case is being actively managed, not passively aging | Demonstrates operational discipline and early-warning systems |

| Historical recovery rate data by attorney and case type | Your portfolio converts at predictable rates with measurable risk profiles | Enables the lender to price the advance accurately and confidently |

| Settlement negotiation timelines and milestone tracking | You know where each case stands in the legal process | Reduces uncertainty around collection timing and portfolio liquidity |

| Case-level escalation protocols for stalled or deteriorating cases | You identify and respond to risk before a case becomes uncollectible | Signals proactive management that protects both your revenue and the lender's position |

How PI Lien Financing Actually Works

You know what makes PI revenue predictable. Now here's how the financing mechanism actually works.

And where most practices misunderstand the structure.

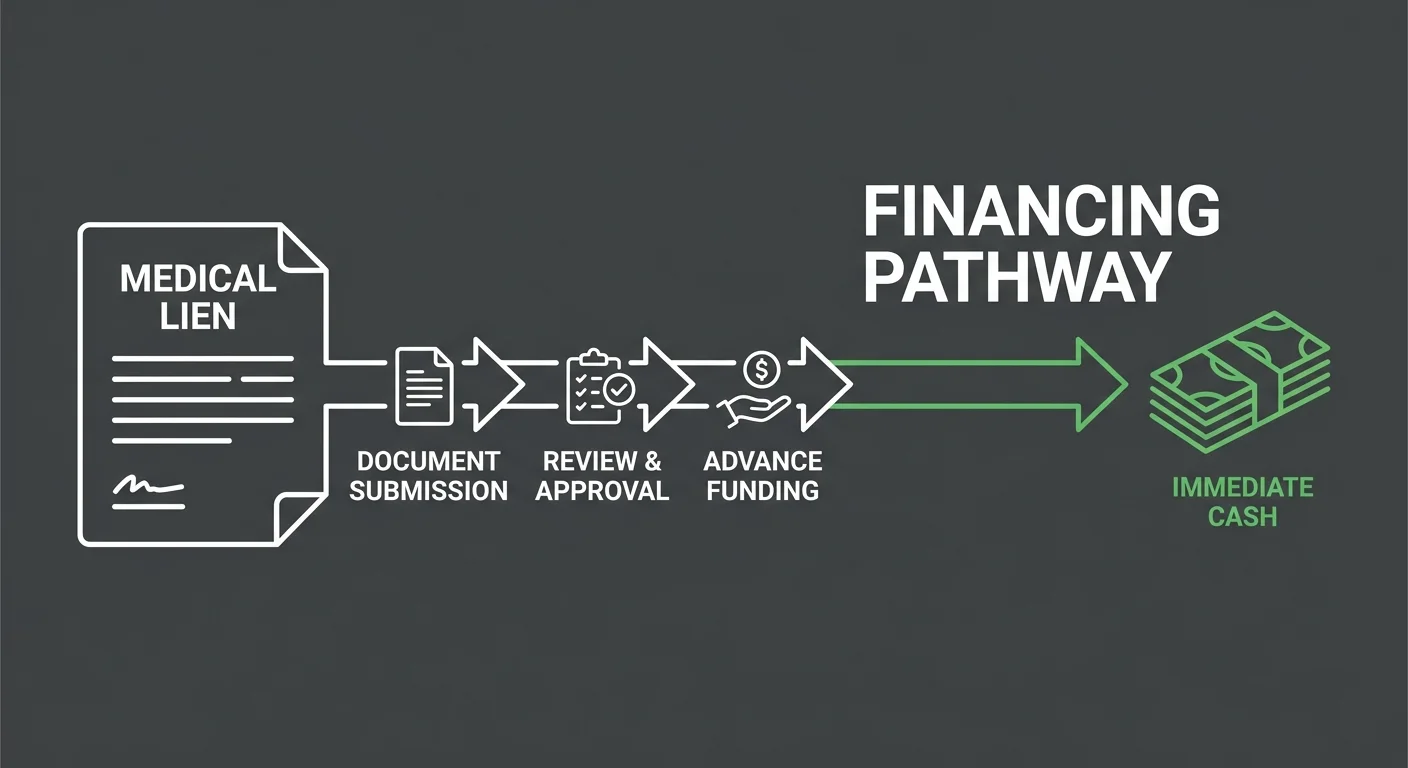

PI lien financing converts your outstanding liens into immediate cash. You sell them to a financing company at a discount. You get working capital now. The lender collects the full lien value directly from the attorney when the case settles.

It's a sale of future revenue. You're not borrowing.

You're monetizing clinical work you've already completed but won't see payment for until the legal timeline resolves.

The financing company reviews your PI portfolio. They assign a value based on case strength and historical recovery data. They offer an advance—typically a percentage of the projected settlement amount.

You accept the capital. The lender assumes the collection risk and waits for the legal timeline to resolve.

Your practice moves forward with expansion capital instead of waiting months or years for settlements to close.

The Non-Recourse Advantage

Most PI lien financing is structured as a non-recourse advance. If the legal case fails—if the patient loses, the attorney withdraws, or the settlement doesn't cover your lien—you don't repay the funds.

The lender absorbs the loss. You keep the capital.

This is different from a traditional loan where repayment is required regardless of outcome.

Non-recourse financing shifts collection risk from your practice to the financing company. Unpredictable legal timelines become predictable expansion capital.

That shift is what makes PI liens work when traditional credit lines don't.

But here's what most practices miss.

Non-recourse doesn't mean the lender takes every case. It means the lender underwrites aggressively on the front end—evaluating case strength, attorney reputation, and your documentation rigor—so they can absorb the risk of occasional losses.

Practices with weak case selection or poor documentation don't qualify for non-recourse terms. They get recourse financing—or no financing at all.

Discount Rates and Face Value

The financing company purchases your PI liens at a discount. If your lien has a face value of $10,000, you get $7,000 in immediate capital.

When the case settles and the lien is paid in full, the lender collects the full $10,000. The $3,000 spread compensates the lender for risk, time, and capital cost.

Discount rates vary based on case quality, time to expected settlement, and your historical recovery performance.

Strong cases with reputable attorneys and short timelines command better rates. Weak cases with uncertain timelines get steeper discounts—or no offers.

The practices that secure the best terms are the ones that can prove their PI portfolio converts predictably. That proof comes from documentation, tracking, and a billing partner who manages PI revenue as a strategic asset—not as aging AR.

Comparing PI Lien Financing to Traditional Practice Loans

Traditional practice loans require credit checks, collateral, and fixed repayment schedules regardless of how your expansion performs.

You borrow against your future income. And you repay whether the expansion succeeds or fails. The loan doesn't care about clinical outcomes or legal timelines.

PI lien financing works differently.

You're not borrowing. You're monetizing revenue you already earned. The capital isn't speculative—it's anchored to completed clinical work tied to legal cases with quantifiable settlement timelines.

And because the structure is non-recourse, you're not personally liable if a case collapses.

Here's the trade-off.

Traditional loans offer lower interest rates because the lender holds collateral and can pursue repayment. PI lien financing offers higher effective costs because the lender assumes collection risk and waits for legal timelines.

The question isn't which option is cheaper. The question is which option unlocks capital you can't access any other way.

For practices with significant PI volume and the infrastructure to document it, medical receivables financing isn't a fallback. It's a strategic lever that turns locked capital into immediate expansion fuel.

| Financing Type | Repayment Obligation | Approval Timeline | Primary Risk |

|---|---|---|---|

| PI Lien Financing (Non-Recourse) | No repayment if case fails—lender absorbs collection risk entirely | Weeks to evaluate case portfolio and documentation; faster than traditional underwriting | Lender assumes legal outcome risk; practice assumes discount cost and case selection quality |

| Traditional Business Loan | Fixed repayment schedule regardless of expansion outcome or revenue performance | Lengthy credit review, collateral assessment, and approval process spanning months | Practice assumes full repayment obligation; lender holds collateral and personal guarantees |

| Line of Credit | Revolving repayment tied to draws; interest accrues monthly on outstanding balance | Moderate—requires established credit history and relationship with financial institution | Practice assumes repayment risk; lender may require periodic financial reviews and covenants |

| Equipment Financing | Fixed payments tied to specific asset; repayment required even if equipment underperforms | Fast approval for asset-backed deals; equipment serves as collateral | Practice assumes technology obsolescence and utilization risk; lender holds lien on equipment |

| Revenue-Based Financing | Flexible repayment as percentage of collections—scales with practice performance | Moderate to fast—based on historical revenue data rather than credit alone | Practice assumes margin compression during repayment period; lender assumes revenue volatility risk |

Structuring Your Expansion Plan Around PI Revenue

Financing unlocks capital. But capital without a plan is just cash you'll burn through.

Start with a business plan that maps financial projections, marketing strategies, and operational changes to your capital timeline. PI lien financing isn't a blank check.

It's a bridge between completed clinical work and settlement. Your expansion plan has to respect that timeline. Or you'll burn through capital before the next financing round closes.

What Expansion Costs Up Front

Expansion hits you with significant upfront capital demands. New equipment, leasehold improvements, and hiring additional staff all require cash before they generate revenue.

Most practices underestimate the gap between expenditure and return.

That gap is where expansion plans collapse.

Equipment financing spreads the cost over time. But it doesn't eliminate the upfront deposit.

Leasehold improvements hit all at once. Staffing requires payroll every two weeks whether your new location is at capacity or not.

If you're using PI lien revenue to fund expansion, you need to know exactly how much capital you're securing. And exactly how much runway that capital buys you before the next settlement check arrives.

And here's what breaks most expansion plans.

Practices calculate capital needs based on best-case timelines. They assume the new location hits 80% capacity within three months. They assume hiring will be smooth. They assume no equipment delays.

When any of those assumptions fail, the capital runs out. And the practice is stuck halfway through an expansion with no way to finish.

Strategic growth for a chiropractic practice requires building financial cushion into every projection—not optimism.

Matching Capital to Timeline

PI lien settlements don't arrive on a schedule you control. They arrive when the legal case closes.

Your expansion timeline has to flex around settlement velocity—not the other way around.

If your PI liens settle within six to twelve months, your expansion plan needs to account for cases that take eighteen. You can't build a rigid timeline around unpredictable legal milestones.

But you can structure your expansion in phases.

Phase one: secure the lease and purchase equipment using your first financing round. Phase two: hire staff and launch marketing once the first wave of settlements closes and you secure a second advance.

Phased expansion matches capital availability to operational milestones. So you're never overextended waiting for a settlement check that's three months late.

Practices that try to fund the entire expansion with one PI lien financing round run out of capital when legal timelines stretch. Practices that phase their expansion around multiple financing rounds stay solvent even when cases take longer than expected.

Building Financial Projections That Hold Up

Financial projections built on guesswork don't survive lender scrutiny.

Financing companies review your expansion plan to assess whether you'll still be operational when your PI liens settle. If your projections assume revenue that doesn't exist yet—or if your cost estimates are vague—the lender sees risk.

And either declines your application or discounts your advance more steeply.

Your projections need three components: documented capital requirements, a realistic timeline that accounts for settlement delays, and a phased rollout that matches expenditure to financing availability.

The business plan must include financial projections and marketing strategy—not aspirational patient volume targets.

Lenders fund plans that demonstrate operational rigor. They decline plans that feel speculative.

So here's the standard.

Your expansion plan should answer this question clearly: if every PI lien in your financing round takes 20% longer to settle than projected, does your practice survive?

If the answer is no, your plan is too aggressive. If the answer is yes, you've built the kind of financial cushion that convinces a lender your expansion is strategic—not speculative.

Steps for a successful practice expansion start with a plan that holds up under stress. And PI lien financing rewards practices that plan conservatively and execute deliberately.

| Expansion Expense Category | Typical Upfront Cost Range | Timing (Month 1-12) |

|---|---|---|

| Equipment (adjusting tables, imaging, therapy devices) | Significant capital expenditure | Months 1-3 (purchase and installation before opening) |

| Leasehold improvements (build-out, signage, ADA compliance) | Varies widely by location condition | Months 1-4 (must be completed before operations begin) |

| Staffing (front desk, billing support, associate DC) | Recurring payroll obligation every two weeks | Month 3 onward (begins before location reaches capacity) |

| Marketing and patient acquisition (digital ads, print, referral programs) | Sustained investment over multiple months | Months 2-12 (ramps up at launch, continues through ramp-up period) |

| Working capital reserve (covering operating losses during ramp-up) | Buffer for delayed timelines or slower patient volume | Months 4-12 (critical for bridging gaps between settlement rounds) |

The Role of a Specialized Billing Partner in Making This Work

You can't turn PI revenue into capital without someone who knows how to work the claims that volume billers abandon.

Here's what that partnership actually does.

A specialized billing partner doesn't just submit PI claims. They manage them as financial assets with measurable settlement timelines. That means tracking case progress. Coordinating with attorneys. Documenting medical necessity. Appealing denials on the high-friction claims that determine whether your PI portfolio qualifies for financing.

Financing companies underwrite based on historical recovery performance. If your billing partner treats PI liens as aging AR instead of strategic capital, your portfolio looks risky. You either get declined or receive a steep discount that erodes your expansion funding.

The billing partner is the difference between PI revenue that sits and PI revenue that converts.

Why Volume Billers Can't Support This Model

Volume-first billing companies optimize for claim submission speed. They're built to process clean claims in high throughput. PI liens break that model.

PI cases require attorney coordination. Lien perfection. Settlement negotiation. Appeals on medical necessity. All work that costs more time than a volume model budgets for.

So the volume biller deprioritizes those claims. They sit. They age.

And when a financing company reviews your PI portfolio and sees liens that haven't been worked in six months, they see risk. Not revenue.

The portfolio doesn't qualify. The capital doesn't unlock. And your expansion stalls because the biller you hired wasn't equipped to manage the claims that matter most.

Here's the tell.

Ask your current biller how many PI liens in your portfolio are actively being worked. Not just submitted. Documented, tracked, and appealed when necessary.

If they can't answer that question in under two minutes with specific case counts, they're not managing PI revenue as a strategic asset. They're processing it like any other AR.

And that's the gap that keeps practices from accessing PI lien financing even when the revenue exists.

The payment timeline can extend for months or even years, creating significant cash flow challenges. A volume biller waits. A specialized partner works the timeline.

What DC-Founded Expertise Brings to the Table

A DC-founded billing partner understands what PI cases actually cost a chiropractic practice. Not just in delayed revenue. In the operational and clinical decisions that strengthen or weaken a lien's enforceability.

Peer authority isn't a marketing angle. It's the difference between a biller who reads a chart and a biller who knows why the attorney asked for that specific documentation. And what happens to the lien if you don't provide it.

Human expertise that automation cannot replace matters most on the claims that financing companies scrutinize hardest.

DC-founded expertise also means understanding the clinical narrative that separates a lien the attorney will fight for from a lien the attorney will negotiate away during settlement.

Financing companies review attorney relationships when they underwrite your portfolio. If your billing partner can't demonstrate strong coordination with the law firms handling your cases, the lender sees friction. And friction translates to discount.

The specialized partner doesn't just recover revenue. They position your PI portfolio as the kind of predictable asset that financing companies will advance capital against at favorable terms.

Performance-Aligned Payment Models

A performance-aligned billing partner gets paid when you do. That alignment changes everything about how PI claims are worked.

Flat-fee billing models treat every claim the same. Because the biller's revenue doesn't depend on whether your practice collects.

Performance-based models tie the biller's compensation directly to your recovery. That means the biller has a financial incentive to work the high-value, high-friction PI claims that take longer and require more documentation. Those are the claims that drive your revenue and theirs.

When you're using PI liens to fund expansion, you need a partner whose economics reward them for maximizing your portfolio's value. Not for minimizing their labor cost per claim.

And here's what that alignment delivers.

A performance-aligned partner tracks every PI case with settlement visibility because their payout depends on the same timeline yours does. They coordinate proactively with attorneys because unresolved liens delay their revenue too. They appeal denials aggressively because a lost claim costs them just as much as it costs you.

The financing is typically structured as a non-recourse advance. The lender absorbs the risk if a case fails.

But the billing partner absorbs operational risk right alongside you. And that shared stake is what convinces financing companies your PI portfolio is managed by someone who treats recovery as seriously as you do.

Performance alignment turns your billing partner into a strategic asset the lender can verify. Not just a vendor you hired.

Frequently Asked Questions

Here's what practices ask when they first hear this model.

These aren't hypotheticals.

They're the exact friction points that separate practices that move forward from practices that stay stuck waiting for settlement checks.

How does funding from PI liens differ from a traditional small business loan?

A traditional loan is recourse debt. You borrow money. You repay it on a fixed schedule. Your practice is liable whether your revenue projections hold or not.

PI lien financing is typically a non-recourse advance. You're not borrowing against your practice. You're selling future PI revenue at a discount.

If the legal case fails and the settlement never materializes, the lender absorbs the loss. You don't repay.

That structural difference means PI lien financing doesn't add debt to your balance sheet. And it doesn't require monthly loan payments that strain cash flow during the expansion ramp-up period.

But here's the trade-off.

Because the lender assumes case risk, the discount on your PI liens is steeper than a loan's interest rate. You're trading lower operational risk for higher capital cost.

The right structure depends on whether your practice can afford fixed loan payments during expansion. Or whether you need the flexibility of capital that only costs you if the underlying cases settle.

What percentage of a PI lien's face value can a practice typically secure as upfront capital?

That depends entirely on how your PI portfolio is managed. And what the lender sees when they underwrite it.

Accounts receivable financing allows practices to sell outstanding invoices at a discount in exchange for immediate working capital. PI lien financing follows the same principle.

But the discount reflects settlement risk, case timelines, and the strength of your billing partner's recovery performance.

A well-managed portfolio with strong attorney coordination and documented case progress commands better terms. A portfolio with aging, unworked liens gets steeper discounts.

Here's what that means in practice.

If your billing partner can demonstrate consistent recovery rates, proactive case tracking, and strong lien perfection, lenders see predictability. Predictability reduces discount.

If your portfolio is full of liens that haven't been worked in months, lenders see risk. Risk increases discount.

The percentage you secure isn't fixed. It's negotiated based on the operational rigor your billing partner brings to the table.

What are the primary risks of using future PI revenue to fund current expansion projects?

The primary risk is timing mismatch.

You're spending capital now to fund expansion. But the PI revenue that funds that capital won't arrive until cases settle. And settlements don't follow your project timeline.

If your expansion plan assumes every case settles on schedule and every cost estimate holds, you're exposed the moment a settlement delays. Or a lien gets reduced during negotiation.

The practices that succeed with PI lien financing build financial cushions into their projections. They phase expansion around capital availability, not optimism. They maintain enough operating reserves to survive delays without stalling the project halfway through.

And here's the second risk.

If you finance expansion against PI revenue but your billing partner isn't working those liens aggressively, the cases don't settle. Your capital doesn't replenish.

You've spent the advance. But the revenue pipeline that was supposed to fund the next phase of growth sits frozen because the claims weren't managed as strategic assets.

The risk isn't the financing structure. The risk is under-resourcing the billing operation that determines whether your PI portfolio performs.

How does a partnership with a specialized billing company impact the ability to secure financing against PI liens?

The billing partner is the operational proof point lenders evaluate when they underwrite your PI portfolio.

Financing companies don't just look at how much your PI liens are worth on paper. They look at who's managing them. And whether that partner has the operational rigor to convert those liens into actual settlements.

A specialized billing partner who tracks case progress, coordinates with attorneys, and works high-friction claims demonstrates that your PI revenue is being managed as a financial asset. Not just processed like aging AR.

That operational credibility translates directly into better financing terms.

But here's what happens when the billing partner is wrong.

If your biller treats PI liens as low-priority AR and doesn't work them proactively, lenders see a portfolio that looks risky. Unworked liens. No attorney coordination. No documentation trail.

That portfolio either gets declined or discounted so steeply that the financing doesn't fund your expansion goals.

The billing partner isn't just a vendor. They're the operational infrastructure that determines whether your PI revenue qualifies as capital.

What documentation is required to prove the value of outstanding PI liens to a lender or financing company?

Lenders underwrite PI lien portfolios by evaluating three things.

The strength of the underlying liens. The operational rigor of the billing partner managing them. And the practice's historical recovery performance.

That means you need documentation that proves each lien is enforceable, properly perfected, and tied to a legal case with a viable settlement outlook.

You need case tracking reports that show your billing partner is coordinating with attorneys and working claims proactively. Not letting them age.

And you need historical data that demonstrates your practice's recovery rates on PI cases over time.

Your expansion plan should include documented PI portfolio performance—not just cost projections and patient volume assumptions.

If your billing partner can't produce that documentation in under 48 hours, your portfolio isn't positioned for financing.

Lenders don't fund speculation. They fund predictability.

And predictability requires operational systems that treat PI revenue as the strategic asset it is.

Where This Leaves You

Your PI lien revenue isn't just difficult AR.

It's captured capital.

Revenue that already exists. Already accrued. Sitting frozen in legal timelines waiting for the right system to release it.

The difference between a practice that treats PI liens as a collection problem and a practice that treats them as strategic capital is the difference between waiting for settlement checks and funding expansion on your own terms.

You can't access that capital without a partner who manages PI claims as financial assets — not aging invoices.

And here's what that shift requires.

You need a billing partner who tracks case progress with settlement visibility. Who coordinates proactively with attorneys. Who works the high-friction claims that volume billers abandon.

You need a performance-aligned structure so your partner's revenue depends on the same recoveries yours does.

You need a business plan that accounts for settlement delays and phases expansion around capital availability — not optimism.

And you need to understand that financing companies underwrite based on how your PI portfolio is managed, not just how much it's worth on paper.

So here's where this leaves you.

If your current billing setup can't answer how many PI liens are actively being worked right now — documented, tracked, appealed — you're not positioned to access PI lien financing.

If your expansion plan assumes every case settles on time and every cost estimate holds, you're not positioned to survive the delays that always happen.

The practices that use PI revenue to fund strategic growth are the ones that stopped treating it like AR and started managing it like the predictable, accessible asset it is.

That's the model. That's the standard.

And that's what separates expansion that stalls from expansion that scales.

Here's where this lands. Your practice has PI liens in your AR right now. You're planning expansion. But you don't know how much of that revenue is recoverable. Or when it'll arrive. You're building on capital you can't see. A practice assessment shows you what your PI portfolio is actually worth. How it's being managed. And whether it's positioned to secure the financing your expansion requires. Schedule a discovery call to see what's sitting in your AR—and what it can fund.

© 2026 Bushido Billing. All Rights Reserved | Web Design by iTech Valet