What is the Difference Between Med-Pay and PI Lien Billing in 2026?

Med-Pay pays you now. A PI lien pays you later.

That's the simplest version. Here's what it actually means for your revenue.

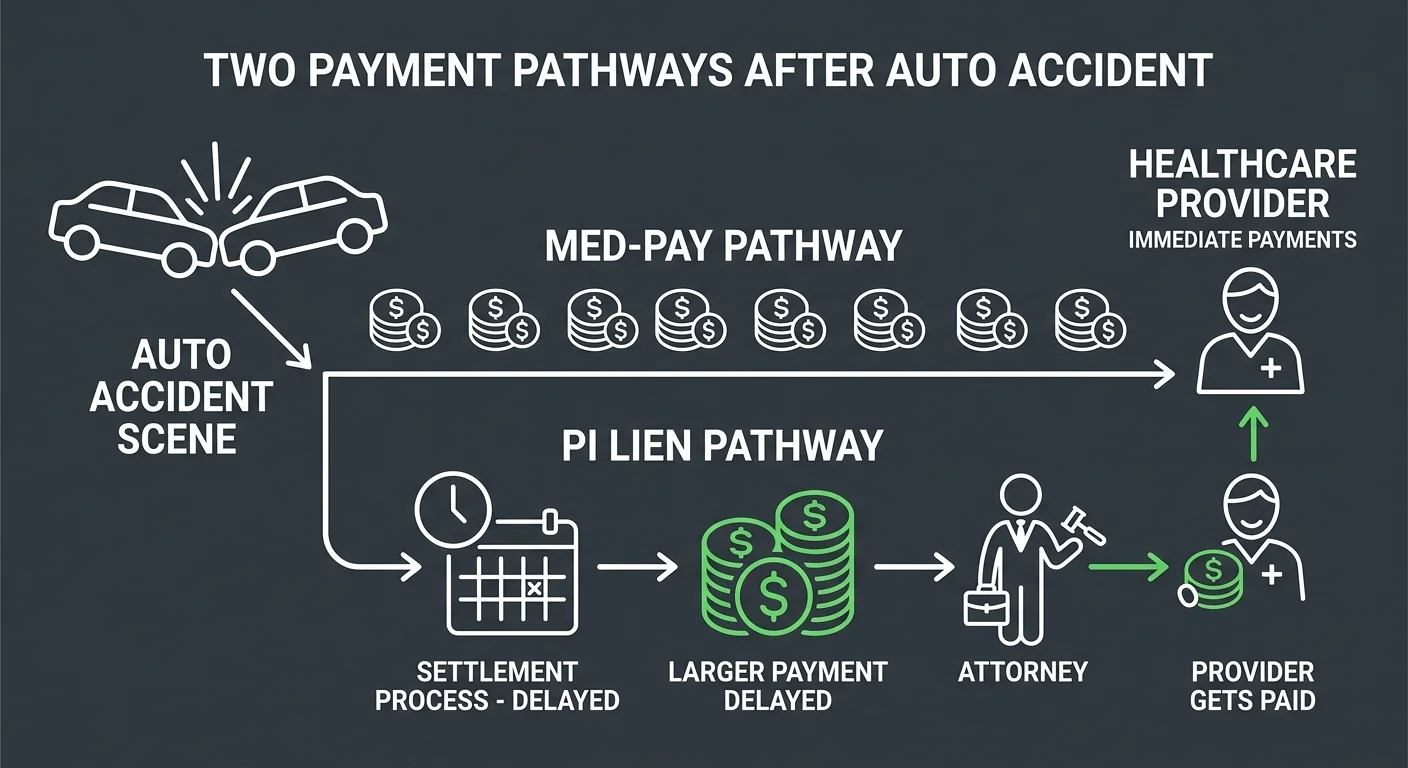

Medical Payments coverage (Med-Pay) is a no-fault benefit within an auto insurance policy. It covers medical expenses for the policyholder and their passengers — no matter who caused the accident. Payment is immediate. No deductible. No copay. But coverage limits run low — typically $1,000 to $10,000. You're paid fast. At reduced rates.

A personal injury (PI) lien establishes a legal claim against a patient's future financial recovery from a lawsuit or settlement. You're paid from those proceeds. Payment is delayed. You wait until the case settles. But you bill your full, standard rates. Med-Pay reimbursements? Those come from a reduced insurer fee schedule.

The choice isn't just about timing. It's about whether your practice gets paid now at a discount — or waits months for full recovery.

But there's another layer. Accepting payment from a Med-Pay policy can grant the auto insurer subrogation rights. That complicates your ability to recover the full value of your services from a final settlement. You bill Med-Pay first. You might lose money later — even if the patient's case wins.

The American Bar Association recognizes medical liens as a mechanism that enables accident victims — particularly those without adequate health insurance — to obtain necessary medical care. For practices treating uninsured or underinsured patients, the lien makes treatment financially viable. The model you choose determines whether you're paid now at reduced rates or later at full value. And whether you're fighting subrogation claims or holding a secured legal position.

Last Updated: May 23, 2026

- What Med-Pay and PI Lien Billing Actually Are

- Payment Timing and Revenue Recovery Potential

- State Law Variables and Subrogation Risk

- Why Most Billing Companies Default to Med-Pay

- When to Use Med-Pay and When to Use a PI Lien

-

Frequently Asked Questions

- What is the core difference in when a provider gets paid with Med-Pay versus a PI lien?

- Can a provider bill both Med-Pay and hold a PI lien for the same patient services?

- How do state laws affect the validity and enforceability of a PI lien?

- Why might a personal injury attorney prefer their client's provider to work on a lien basis instead of billing Med-Pay?

- What key documentation is required to properly file, manage, and collect on a PI lien?

- Does accepting a Med-Pay payment reduce the final settlement amount available for a PI lien?

- Where This Leaves You

What Med-Pay and PI Lien Billing Actually Are

You can't choose between them until you understand what they actually are — not what your last billing company told you they were.

Most practices treat Med-Pay and PI lien billing as interchangeable claim submission paths.

They're not.

They're fundamentally different revenue models with different timelines, different rate structures, and different legal consequences. One pays you now. The other pays you later. But the bigger difference is what you're paid and what rights you're giving up to get it.

The decision you make at intake determines whether you get immediate cash flow at a discount or wait months for full recovery.

That's not a billing question.

That's a revenue strategy question.

Med-Pay: Immediate Payment, Reduced Rates

Medical Payments coverage (MedPay) is a no-fault benefit built into an auto insurance policy. It covers medical expenses for the policyholder and passengers — no fault determination, no deductible, no copay. You bill the patient's auto insurer. The claim processes like standard insurance. Fast, clean, simple.

But Med-Pay reimbursements follow a reduced insurer fee schedule — not your full customary rates.

And accepting that payment can trigger subrogation rights. The insurer gets a legal claim against any future settlement proceeds. You get paid fast, but you don't get paid full value. And in some cases, billing Med-Pay first disqualifies you from recovering the balance through a lien later.

PI Lien: Deferred Payment, Full Recovery Potential

A personal injury (PI) lien establishes a security interest against a future settlement or lawsuit award. You're not billing an insurer. You're establishing a legal claim that ensures your practice gets paid from the patient's recovery when the case settles.

Payment is contingent. If the case doesn't settle or award, you don't get paid from that mechanism.

But if it does, you're holding a secured position.

The advantage is full rate recovery. PI lien billing lets you charge your standard rates — not a discounted fee schedule. The disadvantage is timing. You wait until the case resolves, and personal injury cases can take months or years to settle.

That's a cash flow problem for practices that can't carry the AR.

But for practices that can — or for practices working with attorneys who coordinate well — the lien model recovers significantly more revenue per case than Med-Pay does.

| Payment Model | When Provider Gets Paid | Who Pays the Provider |

|---|---|---|

| Medical Payments (Med-Pay) | Immediately after claim submission — typically within 30 days | Patient's auto insurance carrier |

| Personal Injury (PI) Lien | When the patient's lawsuit or settlement resolves — often months or years after treatment | Patient's settlement or lawsuit award proceeds |

Payment Timing and Revenue Recovery Potential

The payment timing trap isn't about when you submit the claim.

It's about when the money actually arrives — and what you're surrendering to get it faster.

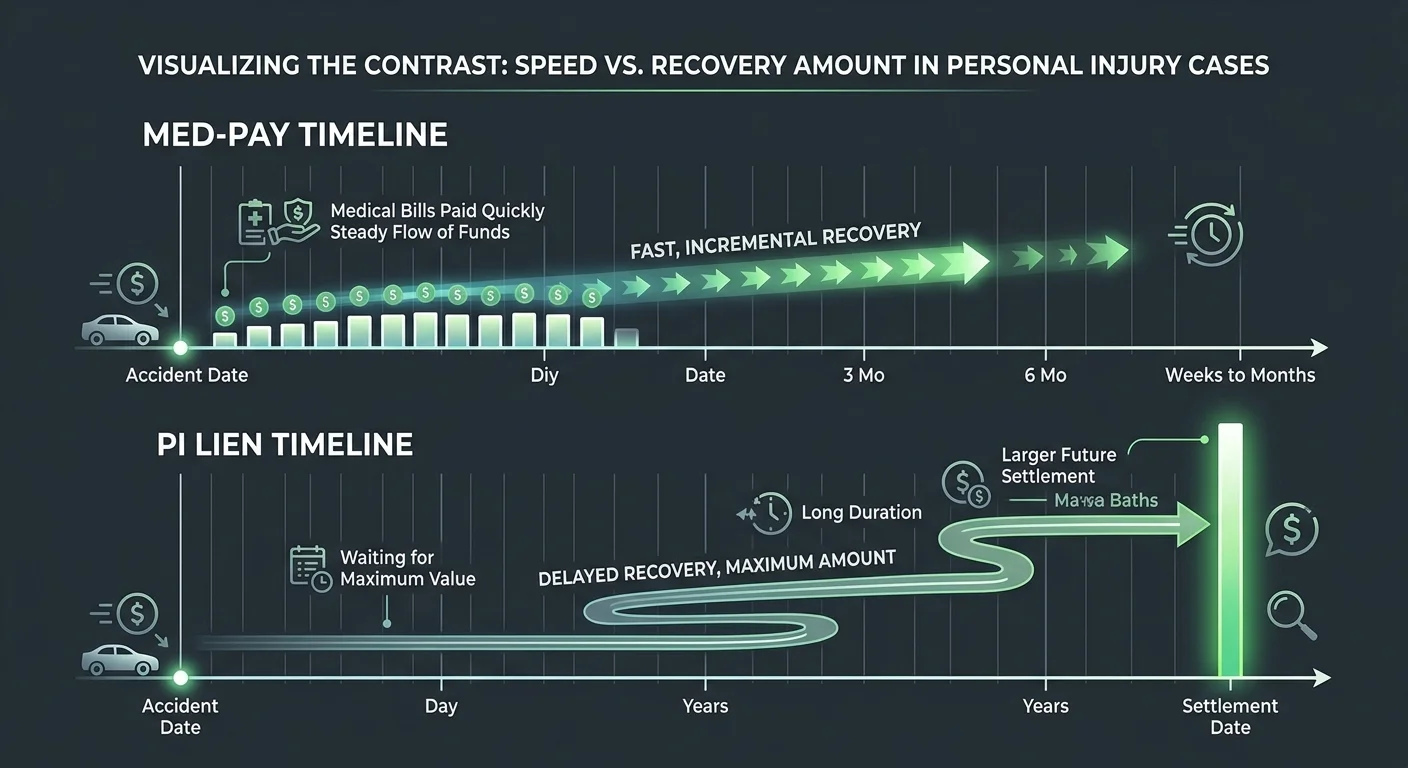

Med-Pay pays fast. PI lien billing pays later. That's the obvious part.

Here's what most practices miss: the speed of payment is inversely correlated with total revenue recovered.

You're not choosing between fast and slow. You're choosing between immediate partial payment and delayed full recovery. Those aren't the same decision.

If your practice can't carry the accounts receivable, Med-Pay makes sense.

If you can wait — and if the case is worth waiting for — Personal Injury (PI) Lien Billing recovers significantly more per case.

But only if you know how to manage it.

Payment Timing

Med-Pay processes like standard insurance. You submit the claim. The auto insurer reviews it. Payment arrives within weeks.

No litigation timeline. No settlement negotiation. No waiting for the attorney to close the case.

The patient's Med-Pay benefit pays you now — regardless of fault or case outcome.

PI lien billing ties your payment to the case timeline. The patient receives treatment. You file the lien. The attorney negotiates the settlement. The case closes. Then you get paid from the settlement proceeds.

That timeline can stretch months or years — depending on the complexity of the case, the jurisdiction, and the defendant's willingness to settle.

Your cash flow waits on variables you don't control.

Revenue Recovery Potential

Med-Pay reimbursements are based on a reduced insurer fee schedule. You don't bill your full customary rate. You bill what the auto insurer's fee schedule allows.

Personal Injury (PI) Lien Billing lets you charge your standard rates. PI lien billing has no fee schedule reduction. No negotiated discount.

Full value.

But accepting Med-Pay payment can trigger insurer subrogation rights. That means the auto insurer gets a legal claim against the final settlement.

That complicates your ability to recover any balance you're owed beyond what Med-Pay paid. In some states, billing Med-Pay first disqualifies you from filing a lien later.

You get immediate payment at a discount, and you lose the legal pathway to recover the difference.

The lien secures your full rate from the settlement. No insurer subrogation fight. No fee schedule cap.

You wait longer, but you recover more — assuming the case settles and the settlement is large enough to cover your lien after attorney fees and other secured claims.

The risk is the timeline and the case outcome. The upside is total revenue recovery.

| Payment Model | Typical Coverage Limits | Reimbursement Rate Structure |

|---|---|---|

| Med-Pay | Commonly ranging between $1,000 and $10,000 | Based on reduced insurer fee schedule |

| PI Lien Billing | No fixed coverage cap — limited only by settlement or award amount | Full customary provider rates |

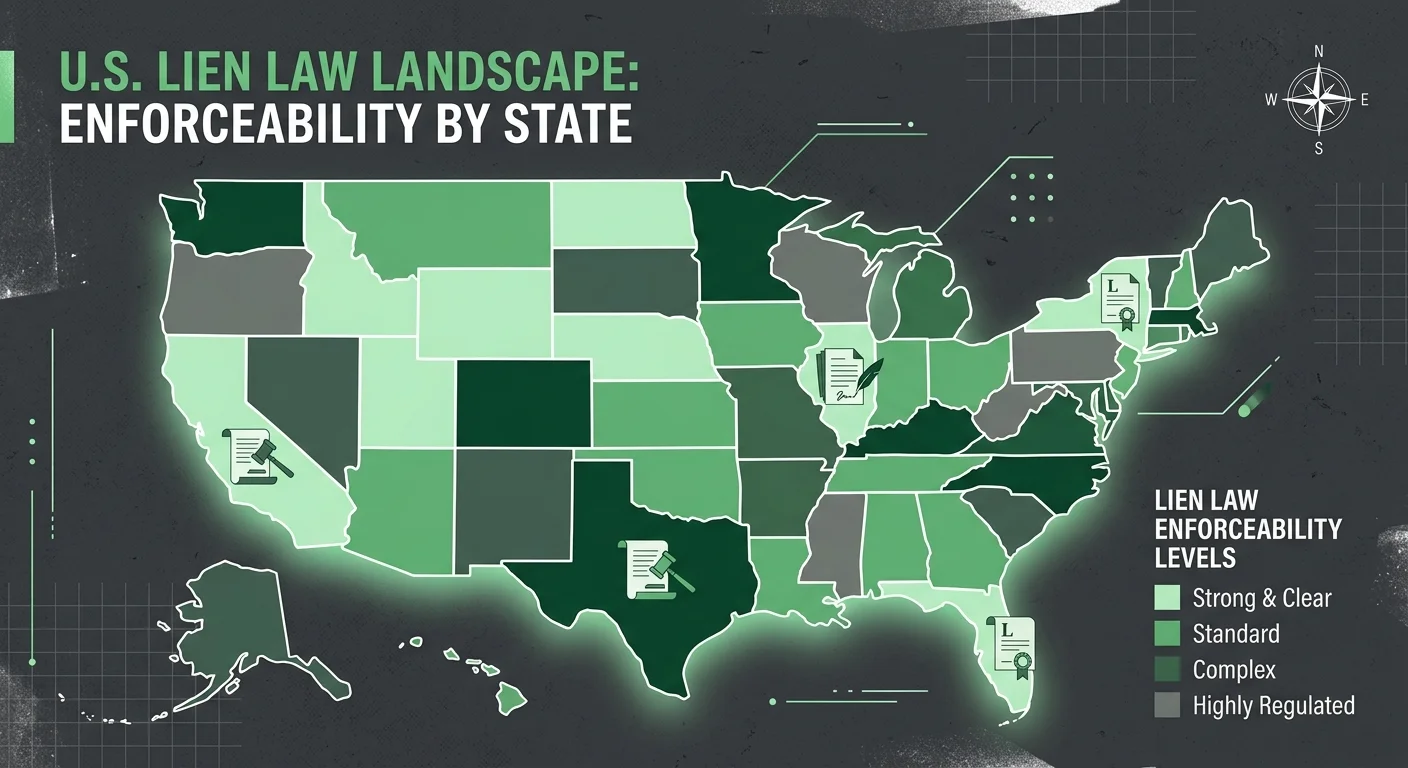

State Law Variables and Subrogation Risk

The decision between Med-Pay and PI lien billing isn't just about payment timing or rate structures.

It's about where your practice operates.

State-Specific PIP and Lien Laws decide whether you can file a lien, whether Med-Pay is mandatory, and whether accepting Med-Pay kills your ability to recover anything beyond it.

These aren't subtle variations. They're structural differences that rewrite the entire revenue strategy.

And if you accept Med-Pay payment without understanding your state's subrogation laws, you're handing the auto insurer a legal claim against your patient's settlement.

That means you're fighting the insurer for money that should've been secured from the start.

State Law Variables

Some states operate under no-fault insurance systems, where Personal Injury Protection (PIP) or Med-Pay is the primary payment mechanism no matter who caused the accident.

In those jurisdictions, you're required to bill the patient's auto insurance first. PI lien billing doesn't become an option until PIP or Med-Pay limits are exhausted. And in some states, it doesn't become an option at all.

Other states let you choose between billing Med-Pay or filing a lien at intake. But the rules still vary.

Some states let you bill Med-Pay and still file a lien for any unpaid balance. Others treat Med-Pay acceptance as a waiver of your lien rights. You don't recover the difference later.

The choice you make at intake is final. And if you don't know the law in your state, you're making that choice blind.

Subrogation Risk When Using Med-Pay

Accepting payment from a Med-Pay policy can grant the auto insurer subrogation rights. That means the insurer gets a legal claim against any settlement or judgment the patient recovers.

The insurer paid your bill. Now they want reimbursement from the settlement. That reimbursement comes out of the patient's recovery. And in cases where the settlement is small, it can consume the funds that would've otherwise covered your lien.

Here's the problem.

If you bill Med-Pay and accept a reduced fee schedule payment, you've lost the revenue gap between your full rate and what Med-Pay paid. And if the insurer exercises subrogation rights, you've also complicated your ability to recover any unpaid balance from the settlement.

The patient's attorney is now negotiating with the insurer's subrogation claim in addition to your lien — assuming you're even allowed to file one after accepting Med-Pay.

You traded immediate partial payment for full recovery. And you gave the insurer a legal tool to block the rest.

Why Most Billing Companies Default to Med-Pay

Most billing companies default to Med-Pay because it's easier to bill.

No lien filing. No attorney coordination. No settlement timeline. No state-specific statute research.

You submit the claim. You wait a few weeks. You collect payment.

It processes like any other insurance claim — same workflow, same portal, same follow-up. Volume-first operations are built for throughput. Med-Pay fits that model cleanly.

But easier to bill doesn't mean better for your practice.

Med-Pay reimbursements follow a reduced insurer fee schedule. You collect partial payment at submission. The revenue gap stays gone.

PI lien billing lets you charge your standard rates — full value, secured by the settlement.

The trade-off is complexity. Lien billing requires personal injury billing and coding expertise, attorney relationship management, and state law compliance.

It's high-friction work. And high-friction work is exactly what volume-first billing models deprioritize.

The Problem With Treating PI Cases Like Standard Insurance Claims

Here's the friction.

PI lien cases don't process like standard insurance claims. There's no clean submission-to-payment loop. You're not billing an insurer and waiting for adjudication.

You're establishing a legal claim that secures your payment from a future settlement. And that settlement timeline belongs to the patient's attorney, the defendant's willingness to negotiate, and the court's docket if the case goes to trial.

Your AR sits open for months or years. Your billing team tracks case status, communicates with the attorney's office, and re-files or updates the lien if treatment extends beyond the initial filing.

That's relationship work, not transaction work. And most billing companies aren't structured to do it.

They're built to move claims through a pipeline at scale. High submission volume. Low per-claim handling time. Automated follow-up sequences.

PI lien billing breaks that model.

Every case requires individualized tracking. Every attorney relationship requires communication cadence. Every state has different filing requirements, notice rules, and priority structures.

You can't automate your way through it. And if you try, you lose liens to missed deadlines, unfiled notices, and attorney offices that stop returning your calls because your billing company never followed up.

So the default becomes Med-Pay. Submit the claim. Collect the reduced payment. Close the case. Move to the next one.

Your practice gets immediate cash flow. The billing company processes the case efficiently.

And the revenue gap between what Med-Pay paid and what a lien would've recovered disappears into the model as an invisible cost — one most practices never see because they don't know what they're losing.

The decision between Med-Pay and PI lien billing gets presented as a simple choice. It's a payment timing trap that determines whether your practice gets paid now at reduced rates or waits months for full recovery.

| Approach | What It Optimizes For | What It Sacrifices |

|---|---|---|

| Med-Pay Submission | Claim throughput and processing speed | Full revenue recovery and long-term practice revenue per case |

| PI Lien Filing | Total revenue recovery and full customary rate collection | Immediate cash flow and operational simplicity |

| Volume-First Billing Model | Low per-claim handling time and automated workflows | High-friction relationship work and individualized case tracking |

| Specialist PI Billing Partner | Attorney relationship management and state-specific lien compliance | Transaction-speed efficiency in favor of recovery accuracy |

When to Use Med-Pay and When to Use a PI Lien

The decision between Med-Pay and PI lien billing isn't a formula.

It's a case-by-case evaluation. Cash flow need, case strength, treatment duration, state law.

Some cases point clearly one way. Others require judgment.

Here's how to make the call.

When Med-Pay Makes Sense

Use Med-Pay when your practice needs immediate cash flow and the patient's treatment costs fall within Med-Pay's coverage limits — commonly between $1,000 and $10,000.

If the case value is low, the liability is unclear, or the patient isn't represented by an attorney, Med-Pay gives you certainty. You're paid within weeks. You're not exposed to the risk of a case that doesn't settle or settles below your lien amount.

Med-Pay also works when state law requires you to bill the patient's auto insurance first before filing a lien.

In no-fault jurisdictions, you don't get a choice. You bill Med-Pay or PIP until those limits are exhausted, then — if your state allows it — you file a lien for the balance.

You start with the auto insurance. If the patient's Med-Pay limit covers your full bill, the case closes there. You're paid. You move on.

When a PI Lien Is the Better Path

File a PI lien when the patient's treatment costs exceed Med-Pay limits, the case has strong liability, and the patient is represented by an attorney.

The attorney's role in managing medical liens becomes your coordination point — they're negotiating the settlement, and your lien is a secured claim against those proceeds.

You're not waiting on an insurer's fee schedule. You're recovering your full customary rate from the settlement.

The lien path also makes sense when accepting Med-Pay payment would trigger subrogation rights that complicate your ability to recover the full balance later.

If your state treats Med-Pay acceptance as a waiver of lien rights, and your bill exceeds Med-Pay limits, you file the lien at intake and skip Med-Pay entirely.

The American Bar Association recognizes medical liens as necessary tools that enable accident victims, particularly those without adequate health insurance, to obtain medical care. It's not a fallback. It's a strategic revenue tool.

Documentation and Attorney Coordination

Whether you bill Med-Pay or file a PI lien, the documentation standard is the same.

Every visit note, every treatment plan, every progress report becomes evidence that supports the medical necessity and value of your services. Weak documentation kills liens. It also kills Med-Pay claims.

But with liens, the stakes are higher — you're not just justifying payment to an insurer. You're defending your claim in a settlement negotiation where the attorney, the defendant's insurer, and every other lienholder is competing for the same pool of money.

That's where attorney coordination separates practices that recover full value from practices that write off balances.

Managing PI cases in a chiropractic practice requires proactive communication with the patient's attorney from intake through settlement. You're not billing the attorney. You're coordinating with them.

They need your documentation to support the demand. You need their case updates to track your lien status. And when the settlement closes, you need to confirm your lien amount is paid in full before the attorney disburses funds.

That doesn't happen automatically.

If you're working with a billing partner, this coordination is their job. If you're handling it in-house, it's yours.

Either way, it's the difference between a lien that gets paid and a lien that gets negotiated down — or ignored — because no one followed up.

Frequently Asked Questions

The questions below surface the real friction points practices face when deciding between Med-Pay and PI lien billing.

You'll see the same objections. The same timing concerns. The same state law confusion.

Here's what you need to know.

What is the core difference in when a provider gets paid with Med-Pay versus a PI lien?

Med-Pay pays you within weeks. PI lien billing pays you from the settlement — months or years later.

Med-Pay is a no-fault benefit. You submit the claim. The insurer processes it. Payment arrives.

A PI lien is a security interest against a future settlement. You file the lien. The case settles. You're paid from those proceeds.

The trade-off is immediate reduced payment versus delayed full recovery.

That's not a billing nuance. That's a revenue strategy decision.

Can a provider bill both Med-Pay and hold a PI lien for the same patient services?

Yes — but the order and state law determine whether it's strategic or self-defeating.

In some states you're required to bill Med-Pay first. Once those limits are exhausted, you file a lien for the balance.

In other states accepting Med-Pay triggers subrogation rights that complicate full recovery from the settlement. If your bill exceeds Med-Pay limits, you skip Med-Pay entirely and file the lien at intake.

It's a case-by-case decision.

And a state-by-state one.

How do state laws affect the validity and enforceability of a PI lien?

Every state has different filing requirements, notice rules, and priority structures.

Some states require you to file within a specific timeframe after treatment starts. Others require written notice to the attorney and the patient.

If you miss a deadline or fail to comply with notice requirements, your lien isn't enforceable.

You've provided the care. The settlement closed. And your claim disappeared because the paperwork wasn't filed correctly.

State law compliance isn't optional. It's what makes the lien collectible.

Why might a personal injury attorney prefer their client's provider to work on a lien basis instead of billing Med-Pay?

Because it preserves more settlement proceeds for their client.

If the provider bills Med-Pay and then pursues the balance as a lien, the insurer's subrogation rights reduce the net recovery. The attorney's negotiating against multiple claims.

If the provider works on a lien from intake, there's no Med-Pay insurer taking a cut.

The attorney controls the settlement disbursement. The provider's lien is a known obligation. And the patient's net recovery is higher.

It's cleaner for the attorney. Better for the patient.

What key documentation is required to properly file, manage, and collect on a PI lien?

Every visit note. Every treatment plan. Every progress report.

They all become evidence of medical necessity and service value.

You also need a signed lien agreement with the patient, written notice to the attorney, and — depending on your state — a filed notice of lien with the court or the defendant's insurer.

Weak documentation kills liens.

Strong documentation defends them in settlement negotiations where your lien competes against other claims for the same settlement pool.

Does accepting a Med-Pay payment reduce the final settlement amount available for a PI lien?

Yes — because Med-Pay is paid from the defendant's policy or the patient's own auto insurance before the settlement is calculated.

If Med-Pay covers part of the treatment, the settlement amount available for your lien is reduced by that payment.

And if accepting Med-Pay grants the insurer subrogation rights, you're now competing with the insurer for settlement proceeds.

That's why some practices skip Med-Pay entirely when the case value and liability support a full lien strategy.

You're not avoiding immediate payment. You're protecting full recovery.

Where This Leaves You

The choice between Med-Pay and PI lien billing isn't theoretical.

It's revenue you either recover or lose.

Here's what most practices don't realize until it's too late: the decision you make at intake determines which number you collect. Bill Med-Pay, and you're locked into the insurer's fee schedule. File a lien, and you're positioned to recover your full customary rate — but only if your billing partner knows how to manage the coordination, documentation, and attorney communication that makes liens collectible.

That's not a claim submission task.

That's a revenue recovery strategy.

Volume-first billing companies default to Med-Pay because it's easier to process.

They're not built for the high-friction work that PI lien billing requires — the attorney relationships, the state law compliance, the settlement tracking, the documentation review.

So they take the path of least resistance.

Your practice absorbs the revenue gap as an invisible cost.

That's not a billing strategy. That's a convenience model dressed up as expertise.

Choosing between Med-Pay and PI lien billing is a critical revenue recovery strategy, not just a claim submission task. It fails under volume-first models. It thrives with a specialist partner who understands that getting paid is the only metric that matters.

You don't need a billing company that processes PI cases.

You need one that recovers PI revenue — and knows the difference.

The payment timing trap doesn't resolve itself. And most practices can't see they're caught in it until the revenue gap shows up in the AR aging report — months after the decision was made. A practice assessment shows you whether your current PI billing structure is recovering full value or leaving money on the table because the coordination, documentation, and attorney communication aren't happening consistently. You're not choosing between Med-Pay and PI lien billing in theory. You're choosing which one actually gets you paid — in full — in your state, with your case mix, under your cash flow constraints.

© 2026 Bushido Billing. All Rights Reserved | Web Design by iTech Valet