How Do State-Specific PIP and Lien Laws Impact Your Practice Revenue?

State-specific PIP and lien laws determine whether your chiropractic practice gets paid for personal injury care. Cross a state line and the entire legal architecture governing that revenue changes.

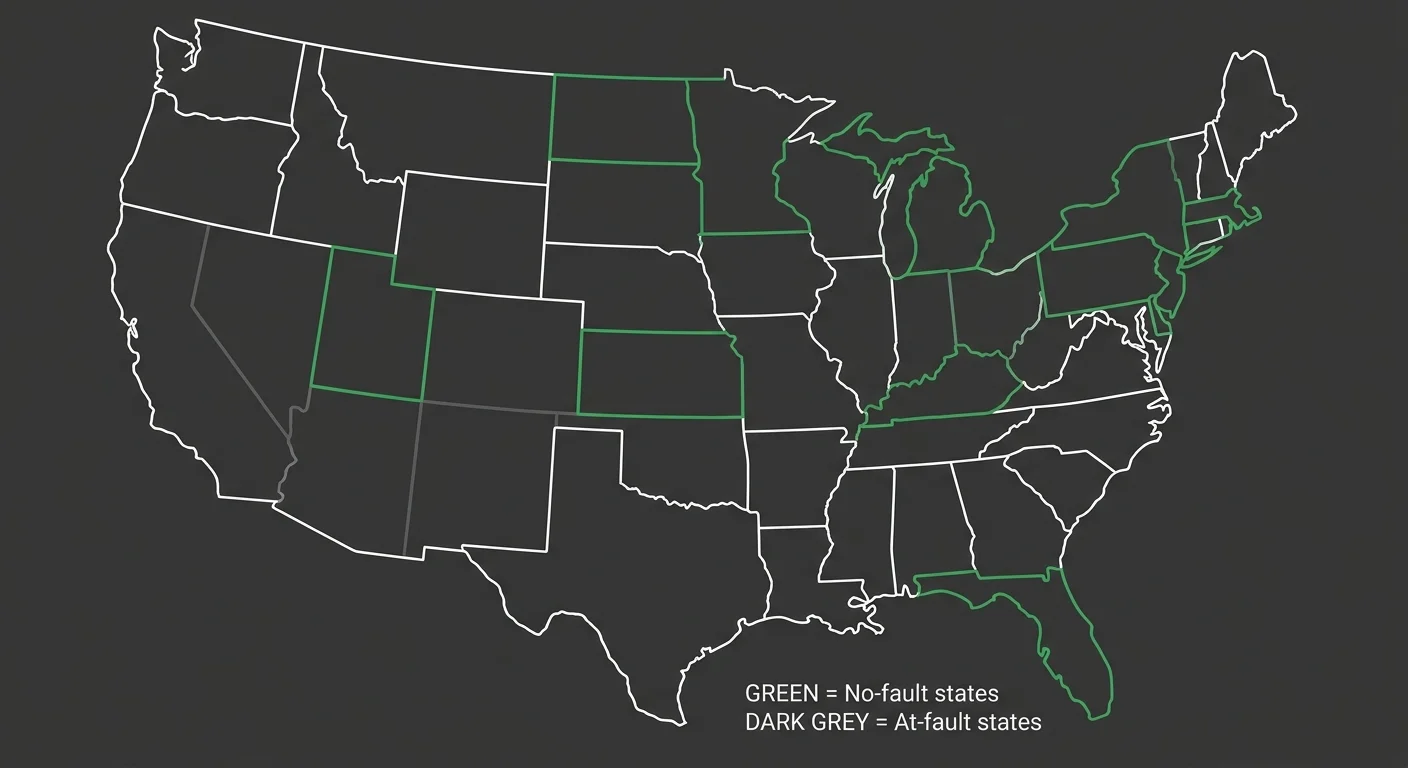

Twelve states, plus Puerto Rico, operate under no-fault insurance systems that require drivers to carry Personal Injury Protection (PIP) coverage. In these states, your billing pathway is dictated by the patient's PIP policy limits before any liability claim or lien becomes relevant. Florida mandates a minimum of $10,000 in PIP coverage. That floor shapes what you bill, when you bill it, and whether you ever need to file a lien.

Outside no-fault states, medical provider liens become the primary recovery mechanism when a patient lacks insurance or their policy is exhausted. But lien laws vary dramatically.

In Texas, you must perfect your lien by filing it with the county clerk in the county where services were performed. Miss that step and your lien holds no legal weight. Other states require formal notice to the patient, their attorney, and the at-fault party's liability insurance carrier to establish validity. Some states offer no statutory lien protections at all. You're forced to rely on a Letter of Protection (LOP), which is a contractual agreement, not a state-granted right.

The specifics matter because they determine enforceability. A lien filed incorrectly or in the wrong jurisdiction is unrecoverable revenue. A PIP claim submitted without the correct AT modifier to designate active versus maintenance care can be denied outright. The state you're in dictates the legal architecture of your revenue recovery. Cross a state line and that architecture changes completely.

Last Updated: May 23, 2026

- The Legal Patchwork: Why State Borders Determine Your Revenue Recovery

- Medical Liens: Statutory Rights Versus Contractual Agreements

- How State-Specific Lien Laws Create Revenue Traps for Practices

- Why Generalist Billers and Automation Abandon These Claims

-

Frequently Asked Questions

- What is the difference between billing under PIP and filing a medical lien?

- Can my practice be forced to accept a reduced payment on a lien during settlement negotiations?

- How does a Letter of Protection (LOP) work if my state has weak or no statutory lien laws?

- What happens to my practice's outstanding medical lien if the patient loses their personal injury case?

- Are there strict deadlines for filing a medical lien after treatment is provided?

- Do PIP exhaustion rules affect my ability to then place a lien on a potential settlement?

- The Cost of Not Knowing Your State's Rules

The Legal Patchwork: Why State Borders Determine Your Revenue Recovery

The United States doesn't have a unified legal framework for personal injury billing. Your practice crosses a state line and the rules governing revenue recovery change completely.

Each state writes its own rules for how providers get paid after motor vehicle accidents. Some states require drivers to carry Personal Injury Protection. You bill that coverage first. Other states operate under at-fault liability models. The patient's own insurance plays no role. You're filing a lien against a future settlement that might never materialize.

Cross a state line and the legal architecture changes completely. The moment your patient's accident occurred in a different state, the rules governing whether your practice recovers revenue shift entirely. Twelve states plus Puerto Rico operate under no-fault systems. The remaining thirty-eight states do not. That border is the difference between a statutory payment obligation and a speculative recovery tied to litigation outcomes you don't control.

What PIP Is and Why It Exists

Personal Injury Protection is mandatory first-party coverage that pays for medical expenses, lost wages, and other costs regardless of who caused the accident. It's designed to eliminate the need for fault determination in routine injury cases.

In no-fault car insurance laws jurisdictions, the injured party's own insurer pays their medical bills up to the policy limit. You bill the patient's PIP carrier directly. No liability claim. No lien. No waiting for settlement.

But PIP limits vary. In Florida, drivers must carry at least $10,000 in PIP coverage. Other states set different floors. Once that limit is exhausted, you're back to filing a lien against any third-party liability recovery—if one exists.

The 12 No-Fault States and Their PIP Requirements

Twelve states plus Puerto Rico require drivers to carry Personal Injury Protection. Those states are Florida, Hawaii, Kansas, Kentucky, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Dakota, Pennsylvania, and Utah.

And each one implements PIP differently. Florida has one set of minimum coverage requirements. Hawaii has another. Kansas, Kentucky, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Dakota, Pennsylvania, and Utah — every single one defines its own rules for exhaustion, its own thresholds for when a patient can step outside the no-fault system and pursue a tort claim. The rules don't travel with the patient.

State-specific PIP coverage limits dictate how much you can recover before you're forced into lien territory. In some states, PIP covers chiropractic care without prior authorization. In others, you need a referral or documentation of medical necessity before the first dollar is paid. The rules aren't portable.

At-Fault States and the Lien-First Model

In the thirty-eight states without mandatory PIP, your revenue recovery depends entirely on the at-fault party's liability insurance — or on the patient's ability to secure a settlement. You're not billing an insurance policy required to pay.

You're securing your right to payment through a medical provider lien — a legal claim against any future settlement or judgment the patient receives. The lien doesn't guarantee payment. It guarantees priority in the distribution of settlement funds. And that's only if the patient wins. And only if there's money left after attorney fees and other liens.

And every at-fault state enforces different lien perfection requirements. Some require county-level filing. Some require formal notice to multiple parties. Some offer no statutory lien protections at all — leaving you with a Letter of Protection, which is a contractual agreement that holds no legal weight outside the patient's consent.

| State | No-Fault or At-Fault | Minimum PIP Coverage | Lien Statute Available |

|---|---|---|---|

| Florida | No-Fault | $10,000 | Yes |

| Florida | No-Fault | $10,000 | Yes |

| Hawaii | No-Fault | Varies by state statute | Yes |

| Kansas | No-Fault | Varies by state statute | Yes |

| New York | No-Fault | Varies by state statute | Yes |

Medical Liens: Statutory Rights Versus Contractual Agreements

A medical provider lien is a legal claim against any settlement or judgment your patient receives in a personal injury case.

That's it.

It doesn't guarantee you get paid. It guarantees you get paid before the patient does—assuming there's money left after attorney fees, other liens, and case expenses. The lien secures your place in the distribution priority.

It doesn't create the money.

But not all liens are created equal. A statutory lien is a right granted by state law. A contractual lien is an agreement between you and the patient.

That distinction determines whether your claim survives a settlement negotiation—or whether it gets ignored the moment the patient's attorney decides it's inconvenient.

Statutory Liens

Statutory liens exist because a state legislature decided healthcare providers treating personal injury patients deserve protection for unpaid services.

They're codified. They carry enforcement mechanisms. And they're not optional for the parties involved.

In Texas, physicians and chiropractors must perfect their lien by filing it with the county clerk in the county where the services were performed. Miss that filing and your lien doesn't exist—no matter how much you billed or how strong your case is.

The law doesn't care about your documentation. It cares about whether you followed the procedural requirements written into the statute.

Other states require formal notice to the patient, their attorney, and the at-fault party's liability insurance carrier before a lien is valid.

That notice isn't a courtesy. It's a legal prerequisite.

Statutory requirements for medical liens vary across jurisdictions, but the pattern is the same: you follow the state's procedural checklist exactly, or your lien holds no weight.

Once perfected, a statutory lien is enforceable.

The patient's attorney can't unilaterally reduce it. The insurance company can't refuse to honor it. It's a legal claim with teeth.

That's the entire point of statutory protection — it removes your revenue recovery from the negotiation table and places it under the protection of state law.

Contractual Liens and Letters of Protection

Unlike statutory liens, a Letter of Protection (LOP) is a contractual agreement, not a right granted by state law. It's a document your patient signs agreeing to pay your bill out of any settlement they receive.

It's critical in states without robust lien statutes—but it's only as strong as the patient's willingness to honor it.

Here's the problem.

A Letter of Protection doesn't bind the patient's attorney. It doesn't bind the insurance company. It doesn't prevent settlement distributions that exclude your bill entirely.

How medical liens are legally enforced depends on whether the lien is statutory or contractual — and contractual liens have no enforcement mechanism beyond a breach-of-contract lawsuit against your own patient.

So you're left chasing a former patient for money they no longer have, after their attorney took a third of the settlement and the liability carrier walked away.

That's not a revenue recovery strategy. That's hope disguised as billing.

The difference between a statutory lien and a Letter of Protection is the difference between a legal claim and a handshake. One survives a contentious settlement negotiation. The other disappears the moment it becomes inconvenient for someone else.

And if you're operating in a state where statutory protections don't exist, understanding the difference between Med-Pay and PI lien billing becomes even more critical—because your revenue depends entirely on which billing pathway you choose and how well you handle the legal gaps your state left open.

| Lien Type | Legal Basis | Filing Requirements | Enforceability |

|---|---|---|---|

| Statutory Lien | Right granted by state law through codified statute | Must file with designated county or state office; formal notice to patient, attorney, and liability carrier typically required | Legally enforceable; cannot be unilaterally reduced by attorney or insurer; survives settlement negotiations |

| Contractual Lien (Letter of Protection) | Voluntary agreement between provider and patient | No government filing required; signed document between provider and patient only | Not legally binding on third parties; attorney and insurer can ignore; enforceable only through breach-of-contract lawsuit against patient |

| Hospital Lien (Statutory Variant) | Separate statutory protection specific to hospital facilities in some states | Filing requirements and notice protocols vary by state; often more favorable deadlines than physician liens | Enforceable under separate statute; may carry different priority in settlement distribution than physician or chiropractic liens |

| Common Law Lien | Implied legal right based on possession of property or records | No formal filing; arises automatically when provider retains patient records pending payment | Weak enforceability in personal injury context; easily circumvented; not recognized in most jurisdictions for medical services |

How State-Specific Lien Laws Create Revenue Traps for Practices

State lien laws don't just vary. They trap revenue by creating procedural requirements that practices miss—and every missed requirement turns billable treatment into unrecoverable loss.

A valid lien filed in the wrong county is worthless. A notice sent three days late is legally insufficient. A modifier left off a claim form voids the entire bill.

The state's rules don't care about your documentation quality or your patient outcomes. They care about whether you followed the procedural checklist written into the statute. Nothing else.

Most practices don't lose revenue because they provided poor care. They lose it because they didn't know the state they were billing in required county-level filing within thirty days. Or formal notice to three separate parties. Or a specific modifier to distinguish active treatment from maintenance.

The clinical outcome was perfect. The billing outcome was zero.

Filing Deadlines and Notice Requirements

Every state with statutory lien protections sets its own filing deadlines and notice requirements.

Miss the deadline and your lien is unenforceable. No exceptions. No extensions. No appeals.

In Texas, you file your lien with the county clerk in the county where the services were performed. If your patient received treatment in Travis County but you filed in Dallas County, your lien doesn't exist.

The statute doesn't recognize good-faith errors. It recognizes compliance.

And formal notice isn't optional. A valid statutory lien typically requires that formal notice be sent to the patient, their attorney, and the at-fault party's liability insurance carrier. That's three separate parties. Three separate addresses. Three separate proof-of-delivery requirements.

Miss one and the lien fails. The patient's attorney won't tell you. The insurance company won't remind you.

You'll find out when the settlement closes without your bill.

Lien Reduction Rules During Settlement Negotiations

Statutory liens protect your right to payment priority.

They don't protect the dollar amount. Settlement negotiations routinely reduce lien amounts—and some states allow it by default.

Here's what happens. The patient's attorney calls and says the settlement is too small to cover all outstanding liens. They propose a reduction.

They frame it as voluntary. But the implication is clear: accept less now, or risk getting nothing if the patient files for bankruptcy or the case collapses.

But the legal enforceability of that reduction depends entirely on your state's lien reduction statutes. Some states allow negotiated reductions if all parties agree. Others protect the full lien amount unless a court orders otherwise.

If you accept a reduction in a state that doesn't require it, you've voluntarily written off revenue you could have legally enforced. Understanding the impact of auto-insurance regulatory changes on settlement patterns becomes critical—because carriers are adjusting their negotiation tactics based on evolving state-level precedents.

PIP Exhaustion and the Transition to Lien Billing

PIP exhaustion is the moment your billing pathway changes—and most practices don't recognize it until the claim is already denied.

In no-fault states, you bill the patient's PIP carrier first. Once that coverage limit is exhausted, you transition to filing a lien against any third-party liability recovery.

But that transition isn't automatic. It requires documentation of exhaustion, updated billing codes, and often a separate lien filing with its own notice and deadline requirements.

And some states don't tell you when PIP is exhausted. The carrier simply stops paying. Your claims sit unprocessed.

By the time you realize the coverage is gone, the lien filing deadline has passed. The revenue is unrecoverable.

The American Chiropractic Association guidelines outline best practices for tracking PIP limits, but enforcement of those practices is the provider's burden—not the insurer's.

The AT Modifier Requirement in Personal Injury Cases

The AT modifier designates active versus maintenance care in Medicare chiropractic billing.

Most practices assume it's a Medicare-only requirement. It's not.

The failure to use the correct AT modifier can jeopardize claim validity, even in personal injury cases. Payers use Medicare billing standards as the baseline for medical necessity determinations across all claim types.

If your documentation doesn't clearly distinguish active treatment from maintenance care, the claim gets flagged. And flagged PI claims don't get paid. They get appealed.

So you're back to arguing medical necessity during settlement negotiations. After the patient's attorney has already agreed to a reduced lien amount. In a state that allows voluntary reductions.

The modifier wasn't wrong. It was missing. And that omission cost you the revenue before the negotiation even started.

| Revenue Trap | Cause | Consequence | How to Avoid |

|---|---|---|---|

| Missed County-Level Filing | Lien filed in the wrong county or missed the jurisdiction where services were actually performed | Lien is legally invalid regardless of documentation quality or bill size | Verify county jurisdiction at intake and file in the county where treatment occurred, not where the practice is located |

| Late or Incomplete Notice | Formal notice not sent to all required parties—patient, attorney, and liability carrier—within the statutory window | Lien fails legal perfection and becomes unenforceable | Send certified notice to all three parties immediately upon lien creation and retain proof of delivery |

| PIP Exhaustion Blind Spot | No tracking system in place to monitor when PIP coverage runs out, so the billing pathway transition is missed | Claims sit unprocessed past the lien filing deadline and revenue becomes unrecoverable | Track PIP limits proactively and trigger lien filing workflow the moment exhaustion is documented |

| Voluntary Lien Reduction in Protected States | Accepting a negotiated reduction in a state where full lien amount is legally protected without court order | Revenue voluntarily written off that could have been legally enforced in full | Know your state's lien reduction statutes before any settlement negotiation and refuse reductions where legal protection exists |

| Missing AT Modifier on PI Claims | Billing without the modifier that distinguishes active treatment from maintenance care | Claim flagged for medical necessity review and payment delayed or denied during settlement | Apply AT modifier consistently across all PI claims and ensure documentation supports active-care designation |

Why Generalist Billers and Automation Abandon These Claims

Here's the pattern: billing companies lose the most revenue on the claims that cost the most time to work.

Those claims also happen to be the most valuable.

High complexity equals high friction. High friction means hours of work per claim. And hours of work per claim breaks a volume-first billing model that measures success by how many claims go out—not by how much money comes back.

The moment a PI claim requires lien perfection, multi-party notice, state-specific filing, or a medical necessity appeal, the generalist biller deprioritizes it.

Not because they don't care. Because their entire operation is built to process clean claims at scale—and complex claims break that scale.

So the claim sits. Then it ages. Then it dies. And your practice never sees the revenue.

Volume Models Deprioritize High-Friction Claims

Volume-based billing operations optimize for throughput. Claims per hour. Submissions per day. Speed is the metric. Revenue recovery is the assumption.

But revenue recovery doesn't follow submission speed when the claim requires work that automation can't handle.

A statutory lien filing in Texas requires county-level research, document preparation, and proof of delivery to three separate parties. That's not a batch process. That's a case-by-case manual task. And manual tasks don't scale in a volume model.

So the volume biller submits the claim once. It gets denied or sits unpaid. They move on to the next hundred claims.

The practice assumes the work is being done. The biller assumes the claim isn't worth the effort. Neither party realizes the disconnect until the aging report shows six figures in unworked PI accounts receivable.

Here's what happens next.

The practice calls. The biller says the claims are 'in process.' The practice waits. Nothing changes. The revenue ages past ninety days, then a hundred twenty, then into the territory where recovery becomes statistically unlikely.

The volume model didn't fail because it was incompetent. It failed because it was never designed to do this kind of work in the first place. Personal injury (PI) lien billing requires a fundamentally different operational model—one that prioritizes revenue recovery over claim velocity.

State-Specific Expertise Requires Human Judgment

Automation handles clean claims. It can't argue medical necessity. It can't read a patient file and craft a nuanced appeal. It can't interpret whether a contractual Letter of Protection holds any enforceability weight in a state with weak statutory protections.

A Letter of Protection is a contractual agreement, not a right granted by state law. That distinction matters when the patient's attorney proposes a lien reduction during settlement.

Software doesn't know whether your state allows voluntary reductions or whether the full amount is legally protected. A human billing specialist does. And that knowledge is the difference between accepting a thirty-percent haircut and enforcing full payment.

The same applies to the AT modifier. The failure to use the correct AT modifier can jeopardize claim validity, even in PI cases.

Automated billing systems flag the modifier as a Medicare requirement. They don't flag it as a medical necessity standard that payers apply across all claim types—including personal injury.

So the modifier gets skipped. The claim gets denied. And the practice loses the appeal before it starts because the documentation didn't establish active care in the first place.

State-specific expertise isn't a software feature. It's human judgment applied to every stage of the billing process—from initial claim coding to lien perfection to settlement negotiation.

Generalist billers don't build that expertise because it doesn't scale across the fifty specialties they serve. Automation can't build it because legal interpretation isn't a programmable task.

That's why how Bushido Billing navigates these complexities comes down to one structural difference: we're specialists, not generalists. We work chiropractic and allied health PI billing every day. We know the state rules. We know the payer patterns. We know which claims are worth fighting and which documentation gaps will kill an appeal before it's filed.

That knowledge doesn't come from a dashboard. It comes from doing the work.

Frequently Asked Questions

You know the structural problem.

You know why generalist billers fail on PI claims.

You know what happens when state-specific rules get ignored.

Here's what practices ask when they realize the system they're using wasn't built for this work.

What is the difference between billing under PIP and filing a medical lien?

Billing under PIP means you submit claims to the patient's own auto insurance carrier. Payment is immediate. It's contractual. The insurer pays up to the policy limit. You bill, you get paid, you move on.

There are 12 states, plus Puerto Rico, that have no-fault insurance laws requiring drivers to carry Personal Injury Protection. If your patient lives in one of them, PIP is your first stop.

Filing a medical lien means you're asserting a legal claim against any future settlement or judgment the patient wins from the at-fault party. Payment isn't immediate. It's contingent. You're waiting for the settlement to close. Then you're competing with other creditors—attorneys, other providers, the patient—for a share of that payout.

The lien protects your right to payment. It doesn't guarantee the amount or the timeline.

PIP is fast but capped. Liens are slow but potentially unlimited. Most practices use PIP first, then file a lien once PIP exhausts. That transition is where the revenue leakage happens.

Can my practice be forced to accept a reduced payment on a lien during settlement negotiations?

It depends on your state. And whether your lien is statutory or contractual.

If your state grants statutory lien rights—meaning the lien is created by law, not by agreement—you generally can't be forced to accept a reduction. The lien amount is legally protected. The patient's attorney can ask. You can refuse. The law is on your side.

But if your lien is based on a Letter of Protection—a contractual agreement—you have less protection. A Letter of Protection is a contractual agreement, not a right granted by state law. That means the patient's attorney can propose a reduction, and whether you accept it is a business decision, not a legal one.

Some states allow voluntary reductions even on statutory liens if the settlement amount is too small to cover all creditors. Others don't. The answer isn't universal. It's state-specific.

And if your billing company doesn't know which rule applies in your state, you'll accept reductions you didn't have to take.

How does a Letter of Protection (LOP) work if my state has weak or no statutory lien laws?

A Letter of Protection is your fallback when your state doesn't grant automatic lien rights.

It's a signed agreement between you, the patient, and often the patient's attorney. You provide treatment now. You accept payment later from any settlement or judgment.

A Letter of Protection is a contractual agreement, not a right granted by state law. That makes it weaker than a statutory lien. It's enforceable, but only to the extent that contract law in your state allows. If the patient's attorney refuses to honor it, you're back to arguing breach of contract—not asserting a legal lien right.

Here's the problem: most practices use LOP templates without understanding what enforceability actually requires. The agreement needs to be signed before treatment starts. It needs clear language about payment priority. It needs acknowledgment from the attorney that they're aware of the obligation.

If any of those elements are missing, the LOP becomes a suggestion, not a contract. And suggestions don't survive settlement negotiations.

In states with weak statutory protections, the LOP is your only tool. That's why getting it right matters.

What happens to my practice's outstanding medical lien if the patient loses their personal injury case?

If the patient loses the case, there's no settlement.

No settlement means no payment source for your lien. Your outstanding balance becomes standard patient debt. You can still pursue collection. But you've lost the protection the lien provided.

The patient is now responsible for the full amount. And most patients who lose PI cases don't have the resources to pay large medical bills out of pocket. That's why they agreed to the lien structure in the first place.

Some practices address this risk by requiring partial upfront payment or co-signing agreements with the patient's attorney. Others accept the risk as part of the PI model. But the risk is real. Not every case settles. Not every settlement covers all creditors.

And if your billing partner doesn't communicate that risk to you upfront, you'll find out the hard way when the aging report shows six figures in unrecoverable PI AR.

Are there strict deadlines for filing a medical lien after treatment is provided?

Yes. And the deadlines are state-specific.

Some states require the lien to be filed within thirty days of the first treatment date. Others allow ninety days, or require filing before the settlement is finalized, or tie the deadline to the date the patient retains an attorney. There's no universal rule.

A valid statutory medical lien typically requires that formal notice be sent to the patient, their attorney, and the at-fault party's liability insurance carrier. Missing any one of those notice requirements—or missing the filing deadline—invalidates the lien.

Here's what makes it worse: some states don't penalize late filing with total loss of the lien. They penalize it with loss of priority. You still have a claim. But you're at the bottom of the creditor list. The attorney gets paid first. Other medical providers who filed on time get paid next. You get whatever's left. In a small settlement, that's nothing.

Most practices don't track these deadlines because they assume their billing company is handling it. Most billing companies don't track them because they're generalists serving fifty specialties across all fifty states. The deadline passes. The lien fails. The revenue is gone.

And no one realizes it until the settlement closes and the check doesn't arrive.

Do PIP exhaustion rules affect my ability to then place a lien on a potential settlement?

Yes. PIP exhaustion doesn't automatically create lien eligibility.

It creates the need for a lien. But whether you can file one—and when—is governed by your state's lien statutes and the timeline of the case.

Some states allow you to file a lien concurrently while billing PIP. Others require PIP to fully exhaust before the lien becomes valid. A few states treat PIP payments as a credit against the lien amount, meaning if PIP paid part of your bill, your lien is reduced by that amount.

And in no-fault states with strong PIP requirements, the lien may only apply to damages that exceed PIP coverage—economic losses, pain and suffering, or long-term care costs that PIP doesn't cover.

The transition from PIP billing to lien filing isn't automatic. It requires updated billing codes, documentation of PIP exhaustion, proof that the patient's coverage is fully depleted, and often a separate filing with its own notice requirements.

If your billing system doesn't track PIP limits in real time, you won't know when to file the lien. And if you file too early or too late, the lien fails. The window is narrow. The stakes are high. And the rules change every time your patient crosses a state line.

The Cost of Not Knowing Your State's Rules

The cost of not knowing your state's rules isn't one denied claim.

It's the pattern.

The PIP claim that dies on your desk because you didn't track coverage exhaustion. The statutory lien that fails because you filed in the wrong county or never sent the notice requirement to the patient's attorney. The settlement negotiation where you accepted a voluntary reduction in a state that legally protects the full lien amount.

Each one looks like an isolated mistake.

But together they're systemic revenue leakage. And no increase in patient volume will offset it.

And here's what makes it worse: you won't see it coming.

The billing company tells you everything's being worked. The aging report shows the accounts as active. The claims sit in limbo for months while deadlines pass and legal protections expire.

By the time you realize the revenue is unrecoverable, the window to fix it is closed.

You're not losing revenue because your practice did something wrong. You're losing it because the system handling your billing was never built for the high-friction, state-specific work that determines whether you get paid.

State-specific PIP and lien laws don't just change your billing pathway — they redefine what counts as competent billing in the first place. A generalist can submit the claim. A specialist recovers the payment.

That's the gap.

Practices that don't track PIP exhaustion timelines lose revenue to expired lien filing deadlines. Practices that don't understand their state's statutory notice requirements lose legal enforceability. Practices that rely on volume-first billers or automation-only platforms lose the high-value claims that require human judgment and state-level legal interpretation.

The solution isn't working harder. It's working with a partner who knows the rules in every state where your patients live — and who treats complex PI claims as the priority, not the exception.

Cross a state line and the legal architecture changes completely. And the law determines whether your practice gets paid.

You already know the problem. You know why generalist billers walk away from the claims that actually matter. The question is whether your AR is bleeding right now from state-specific PIP and lien complexity — and whether anyone's even looking. A practice assessment tells you which claims are still workable, which aren't, and what breaks the moment your next patient crosses a state line. Schedule a discovery call to see where your revenue is sitting — and where it's slipping through cracks you didn't know existed. Every month you wait is another month recoverable revenue ages past the point of return.

© 2026 Bushido Billing. All Rights Reserved | Web Design by iTech Valet